Ten Insights About Older Households from the 2020 State of the Nation’s Housing Report

The changing nature of older adult households and the challenges they face are both highlighted in our new State of the Nation’s Housing report. Here are 10 notable findings from the report, in some instances supplemented with additional analyses from our work.

1. Households age 65 and over are increasing faster than any other age group, both in number and as a share of all households. The number of households aged 65 and over increased by nearly a million each year between 2014 and 2019, lifting the share of older households from 24 percent to 26 percent. In contrast, households under age 45 grew by a total of one million over the same period. Over the next decade, the population age 75 and over is expected to grow from 23 to over 34 million people, an increase of 48 percent.

2. Older households are shaping both ownership and rental markets. In 2019, the national homeownership rate edged up slightly to 64.6 percent according the Housing Vacancy Survey, bolstered in part by the high homeownership rate (78.6 percent) among older households. With growth in the older population, the number of older homeowners increased by more than 2.5 million from 2016 to 2019. But at the same time, the number of older renters has also risen, and adults age 55 and over contributed about two-thirds of rental housing growth from 2004-2019. This age group now constitutes 30 percent of all renter households, and over 13.2 million households.

3. The growing older population is changing the mix of household types. Aging, concerns over the costs of housing and care (of both older adults and children), and growth in Hispanic, Asian, and foreign-born households, which are more likely to include multiple generations, are all contributing to an increase in multigenerational living. The number of two-generation households, consisting of adult children at least 25 years old and their parents, rose by nearly 1.8 million from 2014 to 2019 to reach 13.8 million—accounting for roughly one out of every three households added during that period. Meanwhile, the number of three-generation households—made up of grandparents and their adult children and grandchildren—also grew over the past five years, increasing by just under 200,000 to 4.7 million. Also, growth in the older population is contributing to other household shifts; households age 65 and over drove nearly all of the increase in households consisting of married couples without children and 80 percent of the growth in single-person households.

4. Racial/ethnic disparities in homeownership rates persist among older households. Over the last decade, the homeownership gap between white and Black older households has widened, climbing from 16 percentage points in 2009 to over 19 percentage points in 2016, where it has remained, according to the Current Population Surveys. The white-Hispanic ownership gap is nearly as large and has not changed substantially over the decade. The gap between white and Asian older adults has narrowed somewhat since 2009 but still exceeds 13 percentage points.

5. Older owners are carrying more mortgage debt. The share of homeowners age 65 and over with housing debt doubled from 1989 to 2019, from 21 to 42 percent, while the median outstanding balance rose from $18,000 to $86,000 (both in 2019 dollars) over the same period. Among owners age 80 and over, 27 percent were carrying mortgage debt in 2019, compared with 3 percent in 1989.

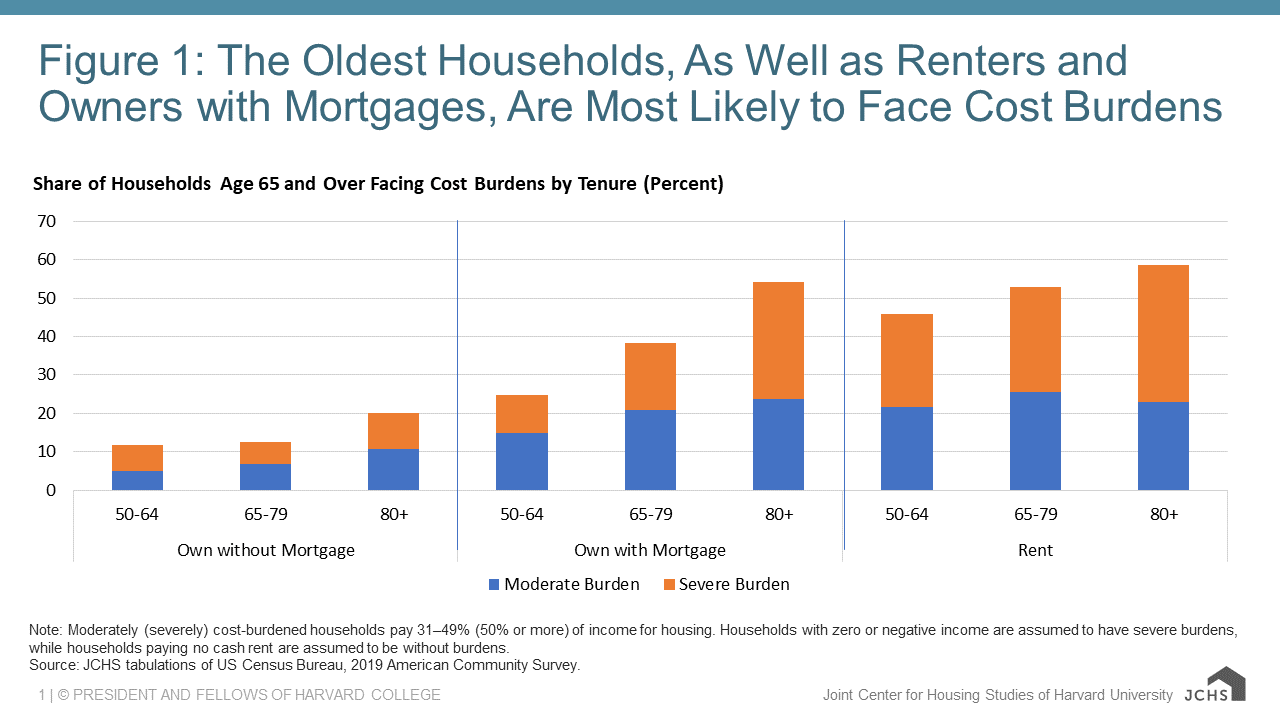

6. Even before the pandemic, a record number of older households were cost burdened. In 2019, the number of older adult households paying more than a third of their income for housing reached an all-time high of 10.2 million. Fully half this group was severely burdened, spending more than 50 percent of their income on housing. Cost burdens are higher at older ages, for renters, and for owners with mortgages (Figure 1).

Figure 1: The Oldest Households, As Well as Renters and Owners with Mortgages, Are Most Likely to Face Cost Burdens

Note: Moderately (severely) cost-burdened households pay 31–49% (50% or more) of income for housing. Households with zero or negative income are assumed to have severe burdens, while households paying no cash rent are assumed to be without burdens.

Source: JCHS tabulations of US Census Bureau, 2019 American Community Survey.

7. Older cost-burdened households often make difficult tradeoffs in their household budgets, particularly if they have low incomes with little residual income after paying for housing. Comparing older households in the lowest expenditure quartile (a proxy for low income), those with severe cost burdens spent an average of $194 per month on food and $174 on out-of-pocket health care expenses, nearly 50 percent less than the $365 spent on food and $345 on healthcare by those who were affordably housed.

8. Many older adults have lost income as a result of the pandemic. Of all age groups, older adults are least likely to report lost wages or falling behind on rent/mortgage since March. Still, nearly 26 percent of renters and 21 percent of owners age 65 and over had reported loss of employment income as of late September’s Household Pulse Survey, and 6.5 percent of older renters and 5 percent of older owners had fallen behind on housing payments, as shown in the interactive chart below. Eviction moratoriums and foreclosure forbearance have helped stabilize housing for those with income losses, but going forward, many older adults will not have housing stability unless they can return to work—and there are uncertainties for older workers, who have faced higher unemployment rates than mid-career workers during the pandemic.

9. In addition to higher risks of serious illness from COVID-19, older adults also face loneliness from social isolation. Older adults are at greater risk of severe illness from COVID-19, and those living in shared housing (such as the 20 percent of older people living in multigenerational settings) may find it difficult to be social distant from household members who are working or attending school outside the home. Yet loneliness, which can be exacerbated by pandemic guidelines, poses its own health risks. While people can be lonely in any setting, risks are higher for those living alone. In 2019, 14 million people age 65 and over lived by themselves, including 4.5 million age 80 and over. As the Center documented in another new report, service coordinators in subsidized, age-restricted housing have sought to support communal life and mental health during the pandemic. But the challenges of loneliness persist as the pandemic wears on, and extend across all housing types and geographies.

10. Funding for rental assistance and development of new affordable housing falls far below need even as the number of eligible older adults increases. HUD reports that in 2017, 39 percent of the nation’s nearly 5 million very low-income older renters faced worst case housing needs, meaning they were paying more than half their income on housing, living in severely inadequate homes, or both. Housing assistance is not an entitlement, and only 38.7 percent of very-low income renters 62 and over received federal rental support as of 2017. There is a need for funding to help build more affordable housing for older adults as well. While some funding for new homes under the Section 202 Housing for the Elderly program was restored in 2018, its budget in fiscal 2020 was still 18 percent lower in real terms than in 2010.

This year’s State of the Nation’s Housing report calls for a national housing policy that would truly address the goal laid out in the National Housing Act of 1949 of “a decent home in a suitable living environment for all.” Part of a comprehensive approach would address the needs of a growing older population, and would include more accessible housing, affordable to those on low and fixed incomes, with an array of options suitable to all types of older and multigenerational households. We also need supportive services and livability features to enable older adults to remain and thrive in their communities. This year, where we live has mattered more than ever; hopefully, our collective experiences will propel us toward a more comprehensive approach to housing.