Renters Vulnerable to Climate Disasters Amid Insurance Gaps

Property insurance is an important tool to support recovery after homes are damaged during weather- and climate-related disasters. However, renter households derive limited financial benefits from property insurance, primarily because they do not own the structures in which they reside. Approximately 41 percent of the nation’s occupied rental stock—more than 18 million units—are in counties considered “high-risk” by the Federal Emergency Management Agency’s (FEMA) National Risk Index. While many renters live in hazard-prone areas, gaps in property insurance markets and public disaster recovery programs can leave renters physically and financially vulnerable when disasters strike.

An estimated 55 percent of renter households nationwide have renters insurance, suggesting that nearly half lack this type of coverage. A standard policy typically covers a tenant’s personal property from a range of perils, but not the building or unit itself. For covered perils, a renters policy may include “additional living expenses” or “loss of use” coverage, which provides funds for temporary housing if the rental unit becomes uninhabitable. However, if a tenant does not have renters insurance or is affected by a peril not covered by standard renters policies (e.g., flood, earthquake), they will not receive a payout to replace damaged personal property nor pay for temporary housing.

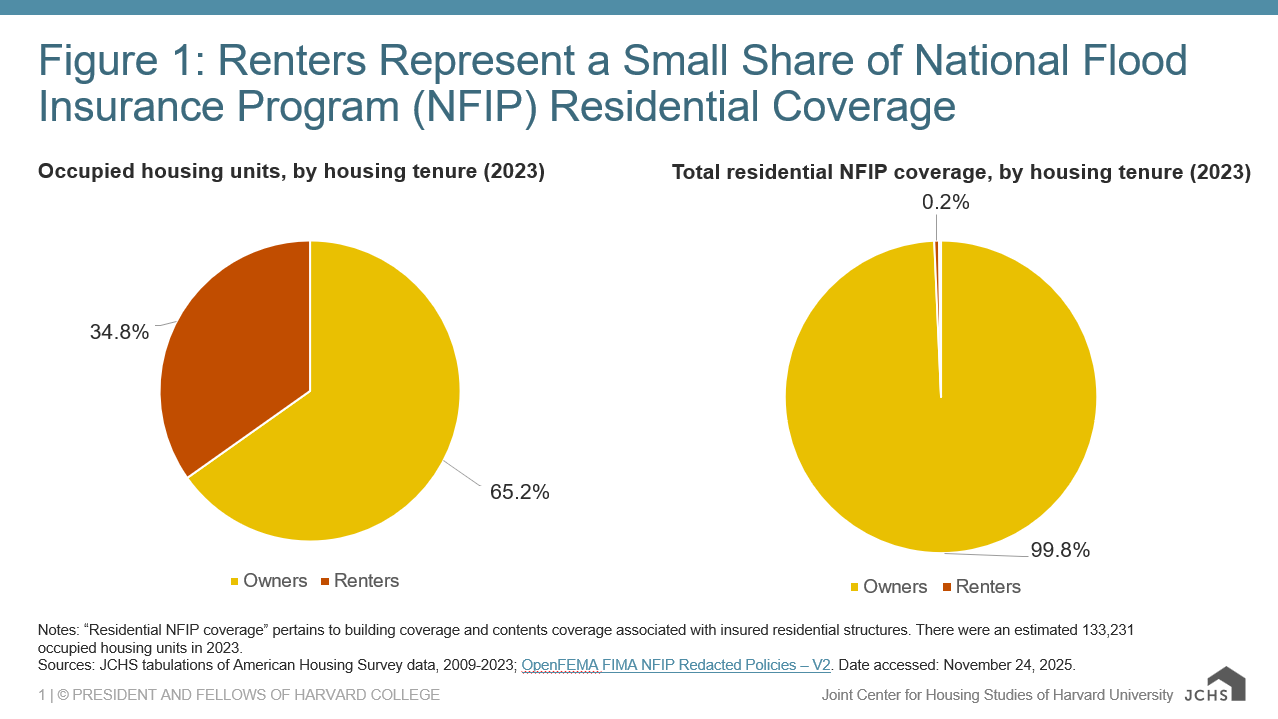

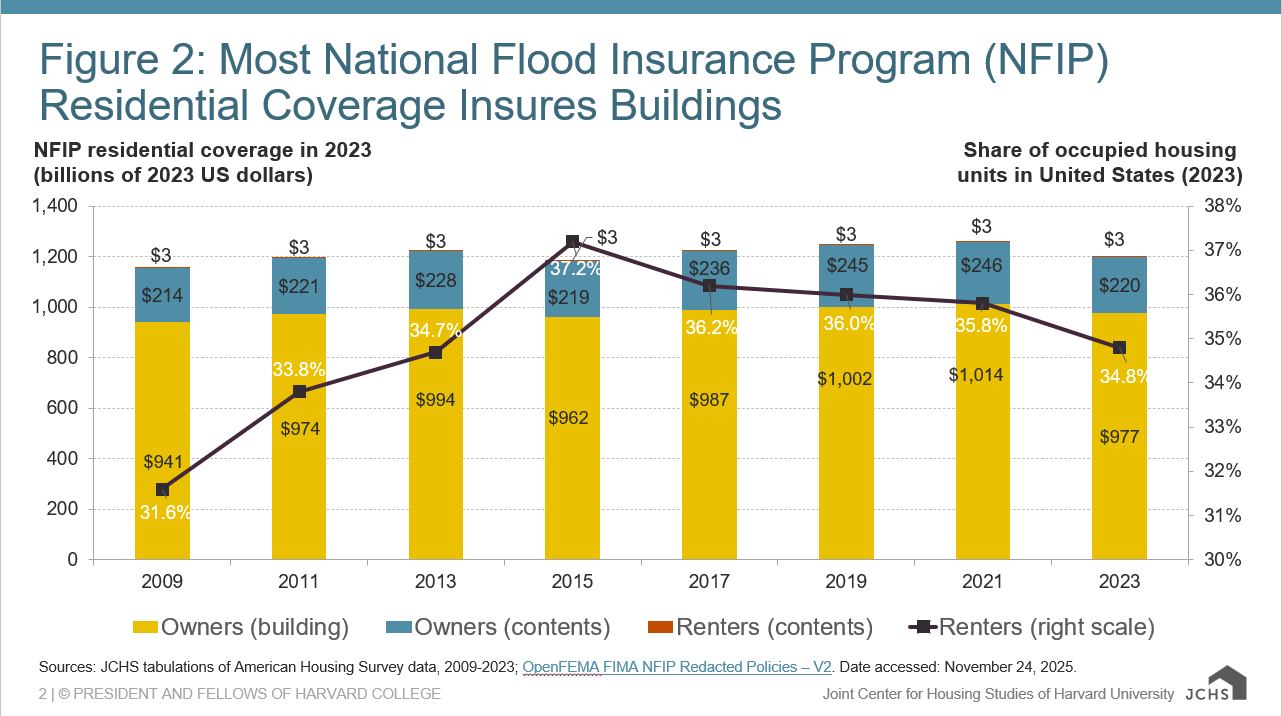

Flooding is one peril not covered by standard homeowners or renters insurance policies. Most flood insurance in the United States is a single-peril policy written through the National Flood Insurance Program (NFIP), which offers both “building coverage” and “contents coverage.” Unlike renters insurance—which can include “loss of use” coverage to pay for temporary housing—the only coverage available to tenants in the NFIP is contents coverage. Figure 1 shows the vast majority of residential NFIP coverage serves building owners. Figure 2 shows a majority of residential NFIP coverage insures buildings.

Figure 1: Renters Represent a Small Share of National Flood Insurance Program (NFIP) Residential Coverage

Notes: “Residential NFIP coverage” pertains to building coverage and contents coverage associated with insured residential structures. There were an estimated 133,231 occupied housing units in 2023.

Sources: JCHS tabulations of American Housing Survey data, 2009–2023; OpenFEMA FIMA NFIP Redacted Policies – V2. Date accessed: November 24, 2025.

Figure 2: Most National Flood Insurance Program (NFIP) Residential Coverage Insures Buildings

Sources: JCHS tabulations of American Housing Survey data, 2009–2023; OpenFEMA FIMA NFIP Redacted Policies – V2. Date accessed: November 24, 2025.

While approximately 34.8 percent of occupied residential units are occupied by renters, only 0.2 percent of all residential NFIP coverage covers renters’ assets or belongings. Research shows the influx of funds provided by property insurance payouts following a disaster can be used to offset not only property damage itself, but an array of ancillary expenses such as temporary housing, evacuation expenditures, vehicle repair, debris cleanup, and landscaping. Since they do not own their residences, renters are not financially responsible for repair or replacement of buildings. However, when flood damages occur, a renter may face an uninhabitable home and limited or no insurance funds to support recovery.

Federal supports, such as FEMA’s Individual Assistance Program, can provide resources to renters for temporary housing in the wake of presidentially declared disasters, but such resources are not always available due to program eligibility criteria. Following Hurricane Helene in 2024, more than 26,600 displaced renter households received support for “transitional sheltering assistance” (i.e., motel or hotel stays) from FEMA. More than 12,100 received rental assistance to pay for alternate rental housing. However, among all renter households registering for FEMA assistance in connection with Hurricane Helene, only 2.6 percent reported having any type of property insurance. This suggests many renter households can expect neither an insurance payout nor federal support during smaller-scale disasters which do not qualify for FEMA aid.

Similar to homeowners, renters are also affected by the rising costs of property insurance. Many landlords are facing rising commercial property insurance costs and passing some of these costs on to tenants in the form of higher rents. This takes place at a time when the number of cost-burdened renters is already at a record high. In a 2023 survey of 418 multifamily housing providers, 58 percent of respondents reported raising rents to manage higher insurance costs. Similar percentages of respondents reported decreasing or deferring other operating expenses and investments in their buildings to offset insurance costs.

Recent large-scale events have only contributed to this challenge. Following the Palisades and Eaton fires earlier this year, the California Department of Insurance (CDI) approved a 38 percent emergency rate increase for “rental dwelling” lines of insurance for the state’s largest property and casualty insurer, State Farm. This increase is higher than CDI’s approved emergency rate increases for State Farm’s homeowners and renters insurance lines, which were 18 percent and 15 percent, respectively. Thus, while renters do not directly pay for property insurance to cover the buildings in which they reside, they are potentially affected by the broader property insurance markets in which their landlords participate.

As affordability challenges and environmental hazards intersect with a warming climate, property insurance is one tool that can manage financial risks from extreme weather events in the future. Since property insurance provides limited direct financial protection to renters, alternative risk management approaches need to be considered to protect renters, such as investments in physical risk reduction, renter-focused financial product innovation, or refinements to existing disaster assistance programs. Rising insurance costs are also putting pressure on affordable housing developers, so upstream interventions that reduce insurance costs for these builders and owners may generate downstream benefits for renters vis-à-vis housing supply and rental prices.