The Landscape of Apartment Property Management

Residential property management companies are important players in the apartment industry, filling a variety of roles to keep properties running smoothly and profitably. Much of the recent focus in policy and academic research has been on the entities that own rental properties, but property managers can be central to the tenant experience, the upkeep of the building, and owners’ bottom lines. In a new working paper, I explore variations in property management company portfolios and the degree to which the industry is concentrated using data from Yardi Matrix that covers properties with at least 50 units. I find that the property management industry is largely fragmented, with almost 12,000 companies operating across the country. Even so, there are several large players that manage hundreds of properties, and companies of different sizes specialize their portfolios by property class and geography.

The majority of property management companies manage fewer than five apartment properties (Table 1). A full 40 percent manage just one property, and an additional 30 percent manage two to four properties. Although most property management companies are small, 107 companies (1 percent) manage at least 100 properties. While few in number, these large companies manage an outsized share of properties and units, accounting for 26 percent of properties in the database and 34 percent of the units.

Table 1: Distribution of Companies, Properties, and Units by Portfolio Size

| Number of Properties in Portfolio | Companies | Properties | Units |

| 1–4 | 8,414 (71%) | 14,495 (14%) | 1,882,927 (10%) |

| 5–19 | 2,542 (21%) | 23,683 (23%) | 3,792,435 (20%) |

| 20–99 | 856 (7%) | 33,347 (32%) | 6,217,590 (33%) |

| 100 or More | 107 (1%) | 26,866 (26%) | 6,317,936 (34%) |

| Owner Managed | – | 5,370 (5%) | 609,156 (3%) |

Source: Tabulations of Yardi Matrix data.

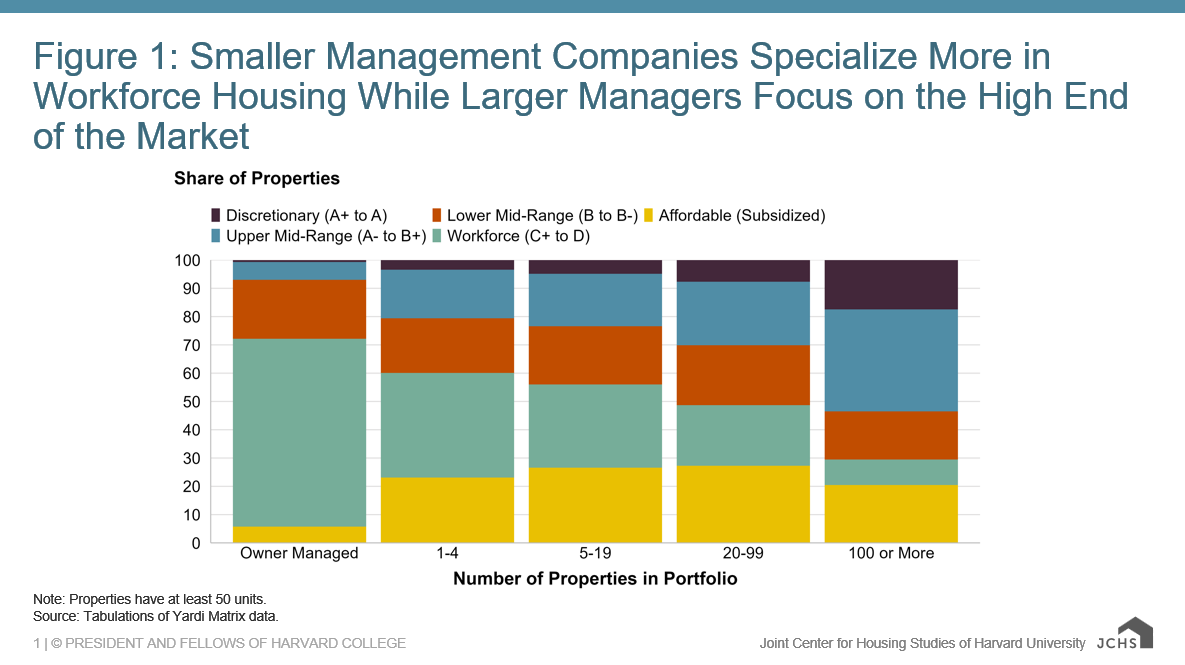

The types of properties that companies manage vary by portfolio (Figure 1). Smaller management companies have a substantial share of their portfolios in workforce housing (rated as class C+ to D) at 37 percent. The share drops as the size of the company increases, down to just 9 percent for companies managing 100 properties or more. Subsidized affordable properties are most common in the portfolios of mid-sized management companies. Just over a quarter of the portfolio consists of affordable housing for companies that manage 5–19 properties (27 percent) and 20–99 properties (27 percent). Larger companies are much more likely to manage high-end properties. Among companies that manage at least 100 properties, 53 percent of their portfolio consists of asset classes rated B+ or higher, including 17 percent rated A or A+. The high-end share of the portfolio is substantially lower for mid-sized and smaller companies.

Figure 1: Smaller Management Companies Specialize More in Workforce Housing While Larger Managers Focus on the High End of the Market

Note: Properties have at least 50 units.

Source: Tabulations of Yardi Matrix data.

Among the largest 25 companies, 15 have portfolios in which more than half of their properties are discretionary or upper mid-range properties rated B+ or higher. With their focus on high-end properties, the 25 largest companies account for 34 percent of all discretionary-rated properties.

A few large companies specialize in affordable, workforce, and mid-range housing. More than 70 percent of the portfolios of The John Stewart Company, The Michaels Organization, and WinnResidential are affordable, subsidized properties. Workforce housing is less common in the portfolios of large management companies, at most making up 46 percent of the portfolios of Monarch Investment and Management Group and 38 percent of the portfolio of the Morgan Properties. These two companies are distinct from the other large property managers in their focus on unsubsidized, low- to mid-range property assets.

The largest 25 companies tend to have geographically dispersed portfolios. Just five companies have 20 percent or more of their properties in a single market, reflecting the fact that most large management companies operate regionally but are not concentrated in specific markets. The top three markets for RPM Living, for example, are all in Texas; the largest three markets for Monarch Investment and Management Partners are in the Midwest; Highmark Residential focuses on Florida markets; and The Michaels Organization is somewhat concentrated in the broader Philadelphia area. The largest company, Greystar Management, has the most geographically dispersed portfolio with just 5 percent of its properties in its primary market, West Houston.

With dispersed portfolios, individual companies make up a relatively small share of most markets. FPI Management has the biggest single market share, managing 13 percent of the properties in Sacramento. A company manages at least 10 percent of apartment properties in just six markets. As the largest management company, Greystar is the primary manager in 12 markets, including Austin, Phoenix, and Raleigh-Durham.

There is some evidence of industry concentration when looking at both asset class and geography. Together the largest 25 companies manage more than 40 percent of the discretionary or mid-range-rated stock in six of their 18 primary markets. The markets with concentrated management of high-end properties include San Francisco, San Diego, and Washington DC/Suburban Maryland. The high-end stock is considerably more fragmented in places like Chicago and Philadelphia. Greystar is the largest company operating discretionary and upper mid-range properties in 12 markets, accounting for an especially large share of high-end property management in San Diego (27 percent), Raleigh-Durham (19 percent), and Salt Lake City (18 percent).

Despite their importance in shaping apartment markets, management companies, the way they operate and hone their portfolios, and the extent to which they are concentrated in certain markets and asset classes is rarely mentioned in policy and research. While this paper is a first step in exploring these dynamics, there are many questions left unanswered. Additional work exploring whether operations and tenant experiences vary by the size and structure of management companies would be useful, as would an examination of how competitive the management landscape is, how these companies market themselves, and how they make decisions about their portfolio composition. It would further be helpful to understand variations in operating costs across different types or sizes of management companies, which would have implications for renter affordability. Additionally, assessing how local regulations and landlord–tenant laws influence the adoption of third‑party property management would be crucial in developing and understanding the tradeoffs of different policies.