Household Mobility Fell to Record Low in 2024

Household mobility fell to its lowest rate on record in 2024, with just over one in ten households moving. Homeowners drove this latest decline as they stayed put in the face of high interest rates and home prices, while renter mobility remained flat as moves into new units were offset by high lease renewal rates. The latest estimates show no substantial change in these factors in 2025, indicating that the past two years reflect a “new normal” of a less mobile nation.

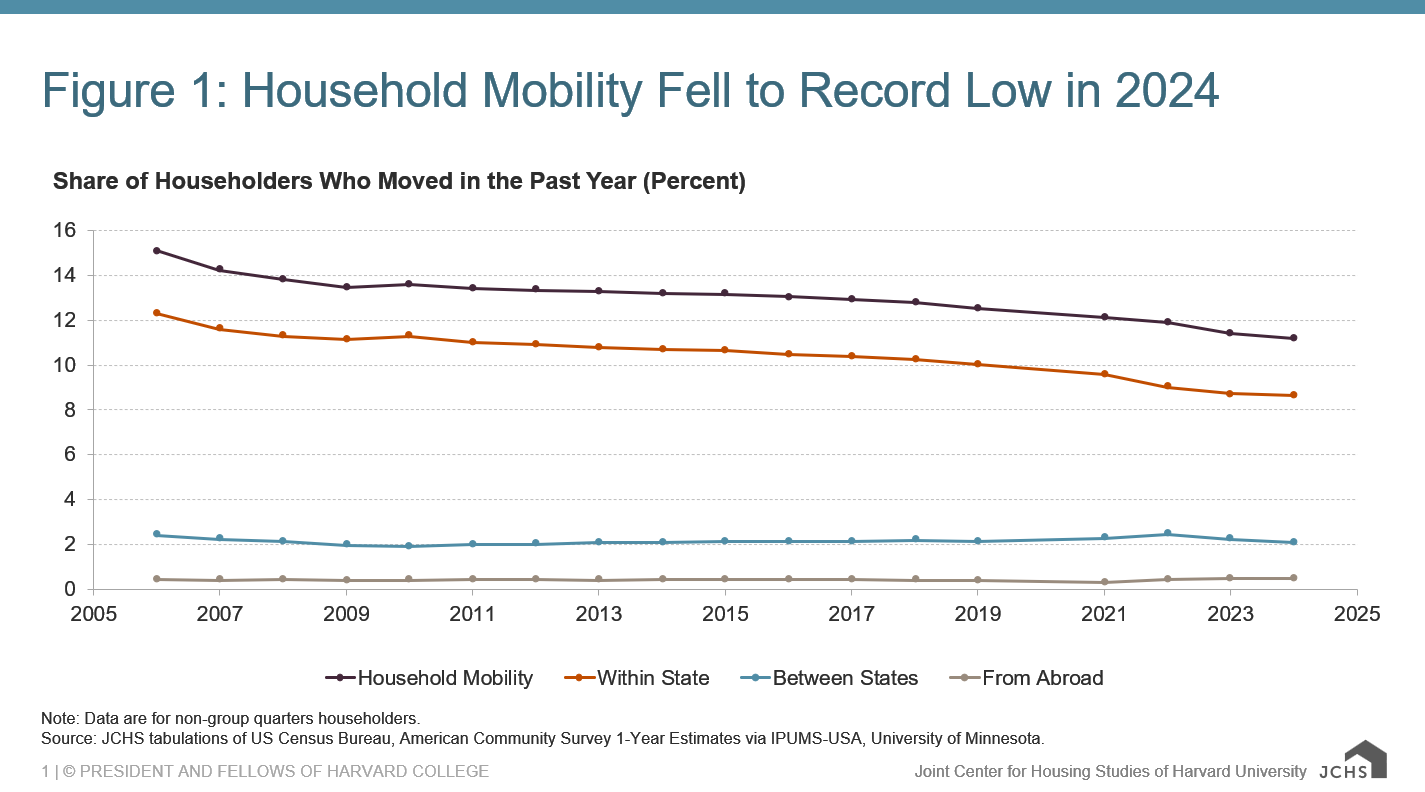

According to recently released American Community Survey (ACS) data, 14.8 million households moved in 2024, representing a mobility rate of 11.2 percent—the lowest on record in this survey (Figure 1). The share of households moving within state—the most common type of move—fell to a record low of 8.6 percent. There were also fewer households moving across state lines after a notable uptick during the pandemic. Household moves from abroad held steady at 0.5 percent from 2023–2024, slightly elevated from previous years due to the surge in immigration—but not reflecting the full magnitude of the surge since new arrivals have low rates of household formation.

Figure 1: Household Mobility Fell to Record Low in 2024

Note: Data are for non-group quarters householders.

Source: JCHS tabulations of US Census Bureau, American Community Survey 1-Year Estimates via IPUMS-USA, University of Minnesota.

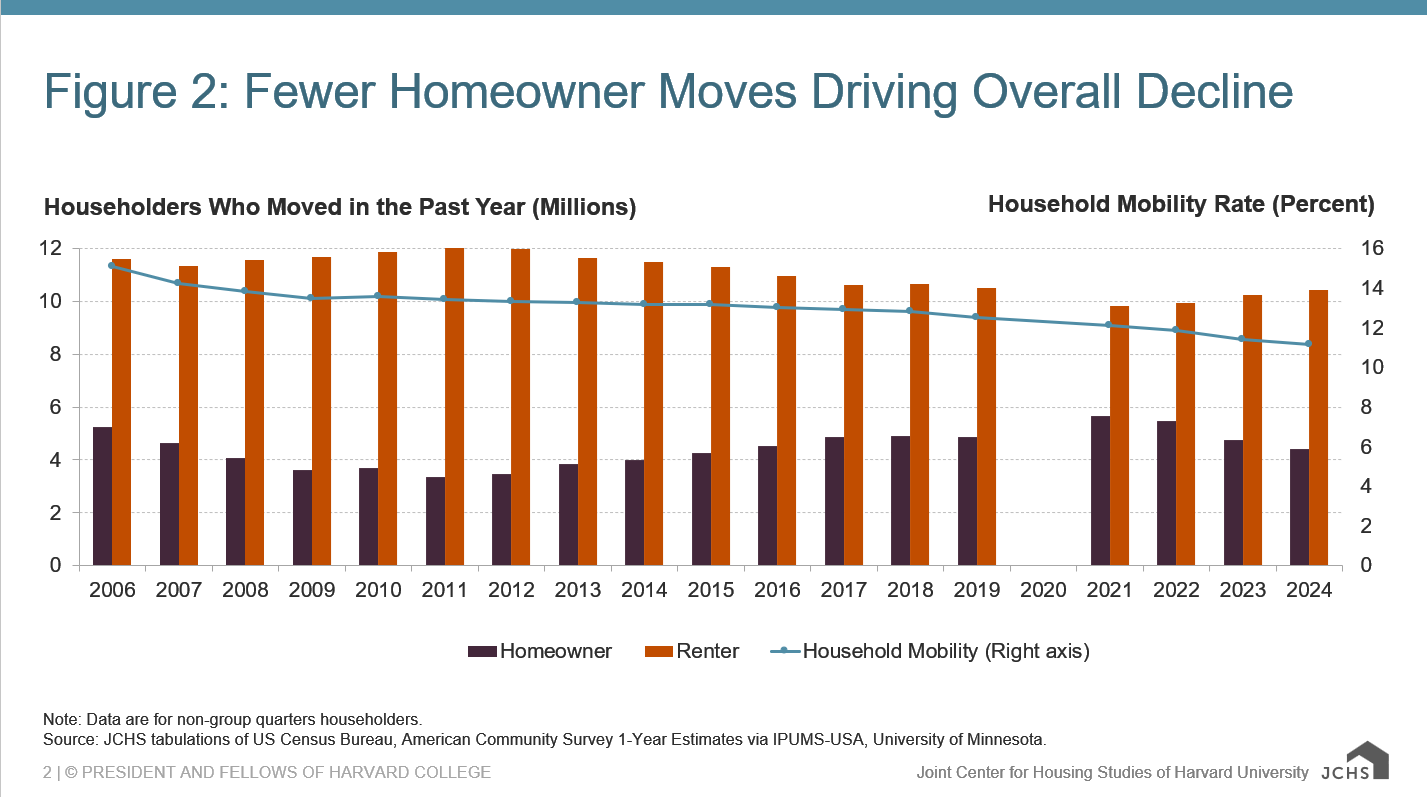

The decline in household mobility was driven by 320,000 fewer homeowners moving as they were disincentivized by high interest rates and home prices (Figure 2). The prevailing 30-year fixed-rate mortgage (FRM) rate averaged 6.7 percent in 2024, and the median single-family home price was a near-record five times higher than the median household income. Consequently, existing home sales totaled 4.06 million in 2024, down slightly from 4.09 million in 2023.

Figure 2: Fewer Homeowner Moves Driving Overall Decline

Note: Data are for non-group quarters householders.

Source: JCHS tabulations of US Census Bureau, American Community Survey 1-Year Estimates via IPUMS-USA, University of Minnesota.

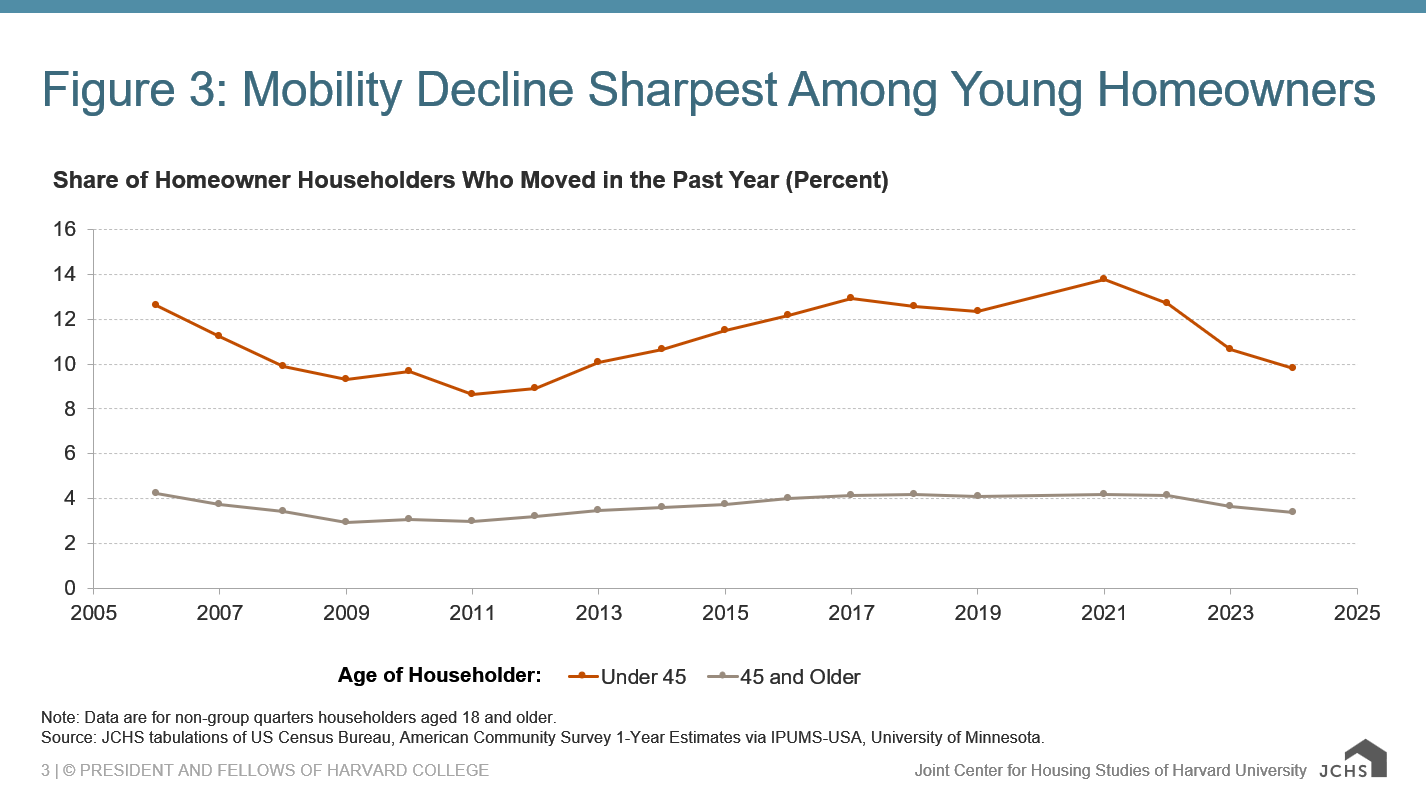

These affordability challenges affected young adults most acutely, many of whom purchased a home during the pandemic. Indeed, from 2019–2021, the household mobility rate of homeowners under age 45 rose from 12.4 to 13.8 percent as interest rates fell and first-time homebuying increased. This mobility rate then dropped as younger homeowners stayed put and fewer households entered homeownership in the next three years. From 2023–2024, the number of young homeowner movers fell by 185,000, pulling their mobility rate down to 9.8 percent (Figure 3).

Figure 3: Mobility Decline Sharpest Among Young Homeowners

Note: Data are for non-group quarters householders aged 18 and older.

Source: JCHS tabulations of US Census Bureau, American Community Survey 1-Year Estimates via IPUMS-USA, University of Minnesota.

In contrast, renter household mobility held steady from 2023–2024. There were an estimated 180,000 more renter household movers in 2024, but their mobility rate was not statistically higher than in 2023. This may be due to the countervailing effects of new rental supply coming online and existing renters renewing leases at a high rate. New rental supply was particularly strong in 2024, with 608,000 multifamily units completed, the highest level since 1986. Absorptions—units going from available to occupied—were also strong, estimated at 550,000, each of which represents a renter household move. However, many existing renters renewed their leases, with the lease renewal rate of large multifamily buildings increasing from 60.5 percent in 2023 to 62.0 percent in 2024, which may have offset the increase in moves into new units.

While these data are from 2024—the most recent available year of the ACS—there is evidence that mobility remained stagnant in 2025. The 30-year FRM rate declined only slightly, hitting its lowest at 6.15 percent and averaging 6.60 percent throughout 2025, which did not substantially improve affordability. Indeed, half of outstanding residential mortgages still had an interest rate below 4 percent in Q3 2025, and existing home sales were the same as in 2024. For renters, lease renewal rates remained high but occupancy rates fell as supply began to outpace demand. Indeed, average advertised multifamily rent was flat in 2025—for the first time since 2020—as demand slowed. This suggests more options for renters to move but no substantial increase in their mobility.

This most recent decline in household mobility is part of a decades-long trend, and the reality today is that many households appear to be “locked in” to their homes. This may mean that households are less likely to seek out better jobs, schools, or housing, limiting their ability to respond to opportunities or shocks. This also limits the flexibility of labor markets, which could contribute to increasing regional economic divergence as opportunity concentrates in high-income communities. The trends may shift quickly, as they did during the pandemic, but without fundamental changes in the housing market, lower household mobility will become entrenched.