Lower Interest Rates Fail to Offset Effects of High Home Prices

The average 30-year mortgage interest rate sits at 6.2 percent, which puts it more than a half percentage point below the 6.8 percent rate averaged in the second quarter of 2025. Nonetheless, homebuying levels remain at 30-year lows, highlighting that it’s not simply interest rates but high home prices that are the major barriers to housing affordability today.

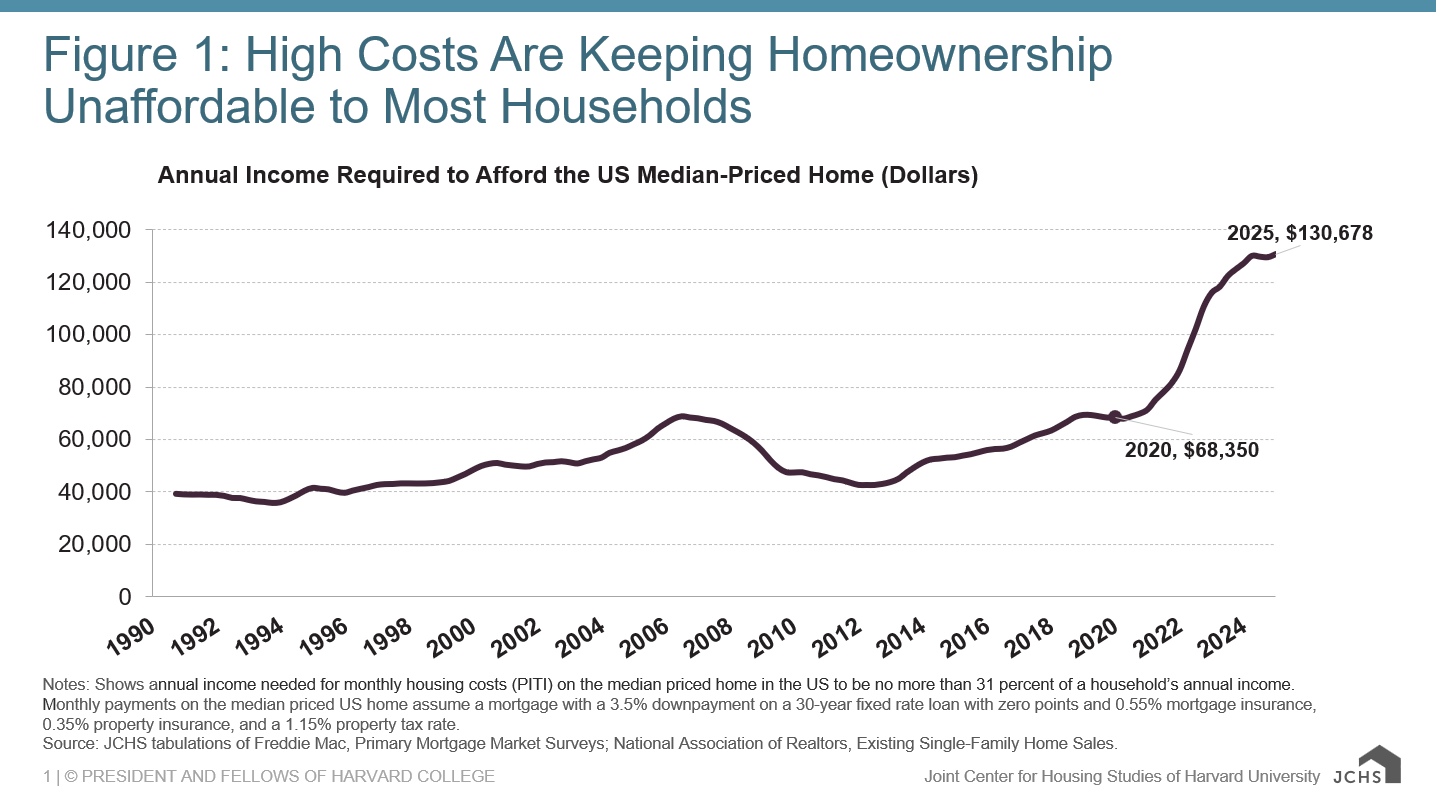

Costs for homebuyers are still historically high. Mortgage payments on the median-priced home in the US are more than double what they were in 2020. For the typical first-time homebuyer loan with a 3.5 percent downpayment, mortgage costs soared from $1,200 per month in 2020 to over $2,500 per month in mid-2025. The annual income needed to afford these costs also nearly doubled from under $70,000 in 2020 to over $130,000 in 2025, pricing out millions of potential homebuyers (Figure 1).

Figure 1: High Costs Are Keeping Homeownership Unaffordable to Most Households

Notes: Shows annual income needed for monthly housing costs (PITI) on the median priced home in the US to be no more than 31 percent of a household’s annual income. Monthly payments on the median priced US home assume a mortgage with a 3.5% downpayment on a 30-year fixed rate loan with zero points and 0.55% mortgage insurance, 0.35% property insurance, and a 1.15% property tax rate.

Source: JCHS tabulations of Freddie Mac, Primary Mortgage Market Surveys; National Association of Realtors, Existing Single-Family Home Sales.

While the 3.2 percentage-point increase in the 30-year mortgage interest rate since 2020 has indeed increased borrowing costs significantly, the current 6.2 percent rate is not abnormally high in historical terms. That is not the case for home prices which, after increasing by 50 percent nationwide since 2020, are at unprecedented heights in nominal terms, real terms, and relative to household incomes. Indeed, the median US home price hit a record five times the median household income at last measure in 2024 (Figure 2).

Figure 2: Compared to Historical Levels, Today’s Home Prices Are More Elevated than Interest Rates

Notes: Price-to-income ratios are based on annual median US home prices and household incomes. Income data for 2024 are based on Moody’s Analytics forecasts.

Source: JCHS tabulations of NAR, Metropolitan Median Area Prices; Freddie Mac PMMS 30-Year fixed rate mortgage, Moody’s Analytics estimates.

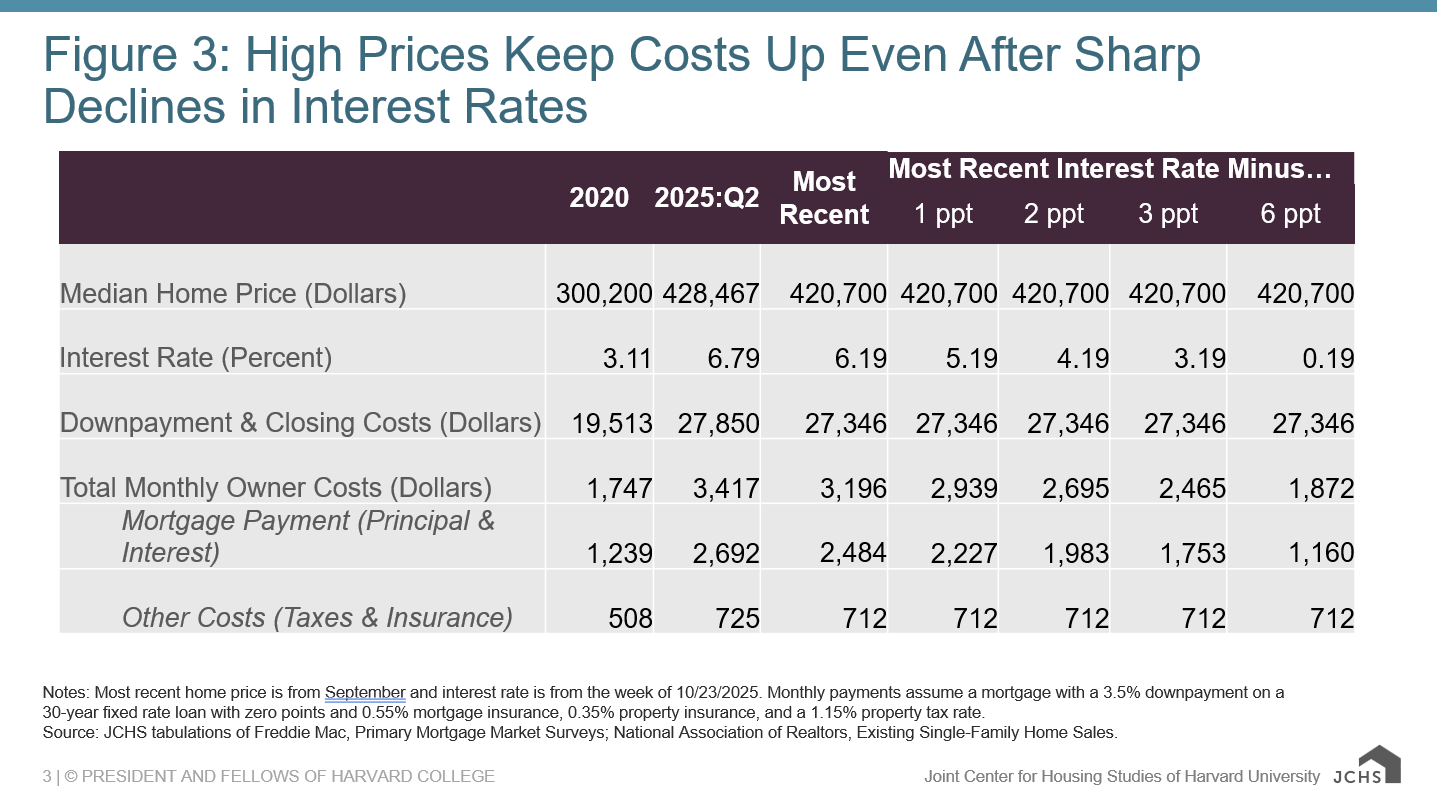

Future interest rate cuts alone won’t restore the affordability lost to the sharp rise in home prices since 2020. The half-percentage point reduction in the interest rate between May and October had the same effect on monthly mortgage payments as a 6 percent decline in home prices. Another full percentage-point decline in interest rates (to 5.2 percent) would reduce monthly payments as much as a 10 percent drop in home prices—helpful, but nowhere near offsetting the impact of the 50 percent surge in home prices since 2020. Most strikingly, it would take reducing interest rates to nearly zero to bring the monthly mortgage payment on the median-priced home back to its 2020 level (Figure 3). But even then, total monthly costs would still be higher than in 2020 due to rising property taxes and insurance premiums.

Figure 3: High Prices Keep Costs Up Even After Sharp Declines in Interest Rates

Notes: Most recent home price is from September and interest rate is from the week of 10/23/2025. Monthly payments assume a mortgage with a 3.5% downpayment on a 30-year fixed rate loan with zero points and 0.55% mortgage insurance, 0.35% property insurance, and a 1.15% property tax rate.

Source: JCHS tabulations of Freddie Mac, Primary Mortgage Market Surveys; National Association of Realtors, Existing Single-Family Home Sales.

Given that interest rates cannot dip low enough to return us to past affordability levels, the most likely path to increased affordability may be for home price growth to slow long enough for household incomes to catch up. But with the affordability gap so wide this could take years. Adding lower-cost units could help speed up the process. The numbers above are based on costs for the typical home. Enhancing the number of smaller or otherwise more moderately priced housing options, such as those traditionally available for first-time, entry-level homebuyers, could help keep homeownership affordable. Since 2010, starter homes, condos, and manufactured housing have been built at levels well below those from the past but could be better encouraged through state, local, and federal policies.

The decline in interest rates is a positive step for millions of potential first-time homebuyers facing historically low affordability. But for homeownership to be attainable in the long term, far more needs to be done to increase the supply of modestly-priced homes affordable to those with median incomes.