Two-Thirds of Working-Age Renters Struggle to Afford Basic Needs

Rising rents are squeezing renter households, leaving them with less residual income to pay for other needs. But inflation has also pushed up the cost of other necessities, making it even harder for renters to afford a modest but adequate standard of living. In a new working paper, we estimate how many working-age renter households face these residual income housing cost burdens—that is, not having enough income left after paying rent to cover all other necessities. We find that about two-thirds of working-age renter households have residual income cost burdens, much higher than the 50 percent with traditional housing cost burdens.

A residual income approach complements the standard 30 percent of income housing cost burden measure and illustrates the different kinds of affordability challenges that renters face. While housing is the largest expense for the typical renter, the high cost of other necessities also squeezes households. This leaves them with difficult decisions to make: cut back on vital needs and sacrifice a modest standard of living or borrow to cover basic expenses? Both options have critical long-term consequences for the financial, physical, and mental well-being of renter households.

We build on our previous work, again using the Economic Policy Institute’s Family Budget Calculator to estimate non-housing expenses for renter households with people under age 65. We omit older adults because they often have more complex healthcare needs that the calculator does not account for. Pairing the calculator with data from the American Community Survey enables us to examine the extent of residual income cost burdens across different household types and geographies and over time.

Housing is the largest single expense for renter households, averaging just over $18,000 annually for the renters in our sample. The combined estimated cost of transportation, taxes, healthcare, food, childcare, and other miscellaneous necessities reaches $57,000 for the typical renter household. These costs make it difficult for all but the highest-income renters to afford rent and basic needs. More than 90 percent of renters making up to $45,000 fall short of the estimated cost of a modest standard of living (Figure 1). But across all income categories, the residual income cost burden measure captures a larger share of households with affordability challenges than the standard housing cost burden measure. Overall, 5.3 million renter households have residual income cost burdens but are not represented in the standard cost burden measure.

Figure 1: The Two Cost Burden Measures Differ Most for Middle-Income Renter Households

Notes: Households have residual income cost burdens if their income does not cover housing and all other estimated expenses. Households with standard cost burdens spend more than 30 percent of their incomes on rent and utilities. Non-cash renters are assumed to not have standard cost burdens.

Source: Tabulations of US Census Bureau, 2023 American Community Survey 1-Year Estimates with Missouri Census Data Center data and Economic Policy Institute, Family Budget Calculator data.

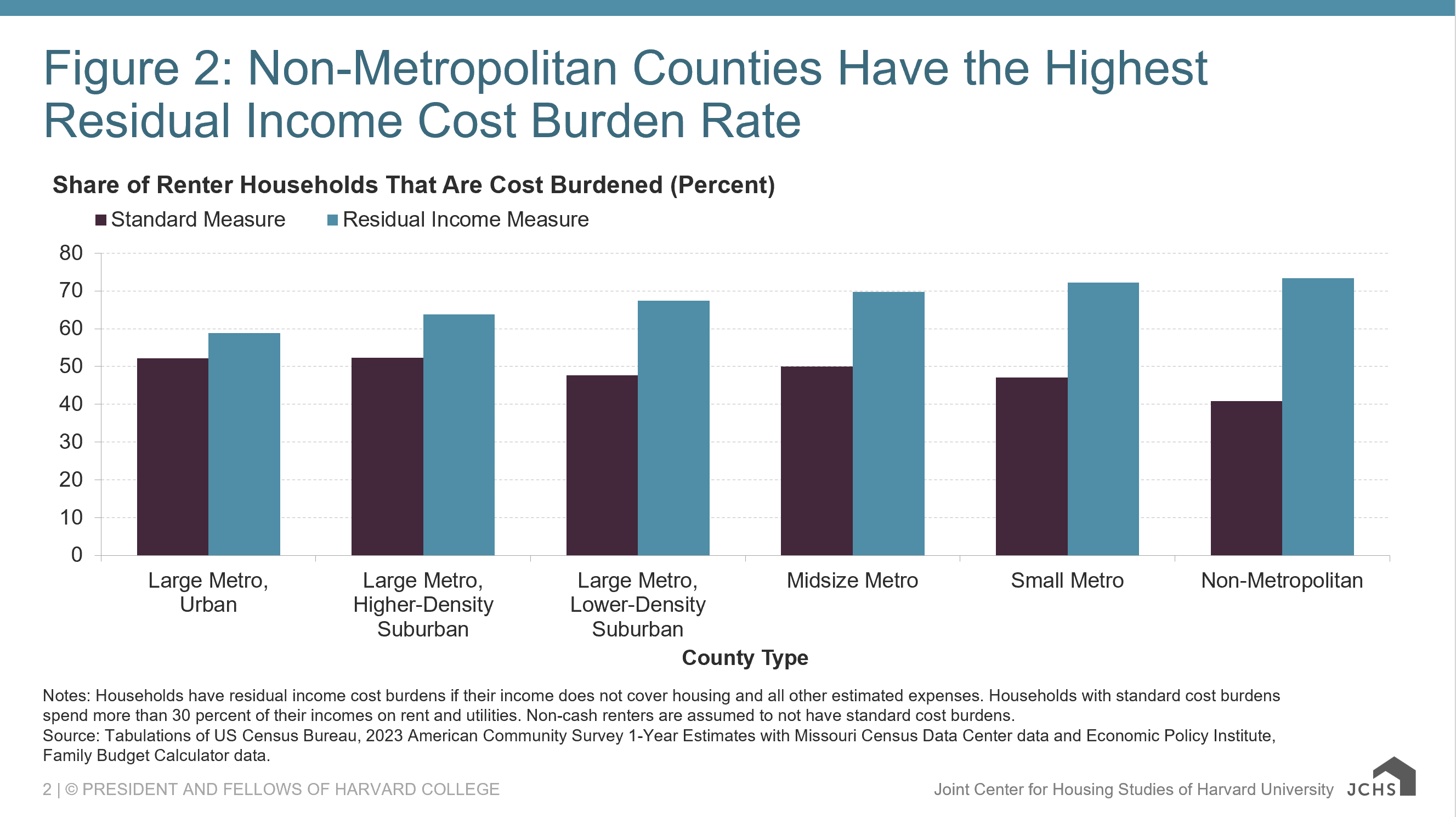

The residual income measure also points to an expanded geography of affordability burdens. Lower-cost states such as Arkansas, West Virginia, and Wyoming have some of the highest residual income burden rates in the country but don’t make the list of states with the highest housing cost burden rates. On the other hand, California, Colorado, and Massachusetts have relatively low residual income burden rates despite average estimated expenses exceeding $80,000 and are among the states with high cost burdens by the traditional measure. Similarly, large urban counties have the highest housing cost burden rate while non-metropolitan areas have the lowest rate. The relationship is flipped for residual income cost burdens (Figure 2). These geographic differences reflect the fact that incomes are too low in some lower-cost states and rural areas to cover rent and estimated basic needs.

Figure 2: Non-Metropolitan Counties Have the Highest Residual Income Cost Burden Rate

Notes: Households have residual income cost burdens if their income does not cover housing and all other estimated expenses. Households with standard cost burdens spend more than 30 percent of their incomes on rent and utilities. Non-cash renters are assumed to not have standard cost burdens.

Source: Tabulations of US Census Bureau, 2023 American Community Survey 1-Year Estimates with Missouri Census Data Center data and Economic Policy Institute, Family Budget Calculator data.

What Would It Take to Meaningfully Reduce the Residual Income Burden Rate for Renter Households?

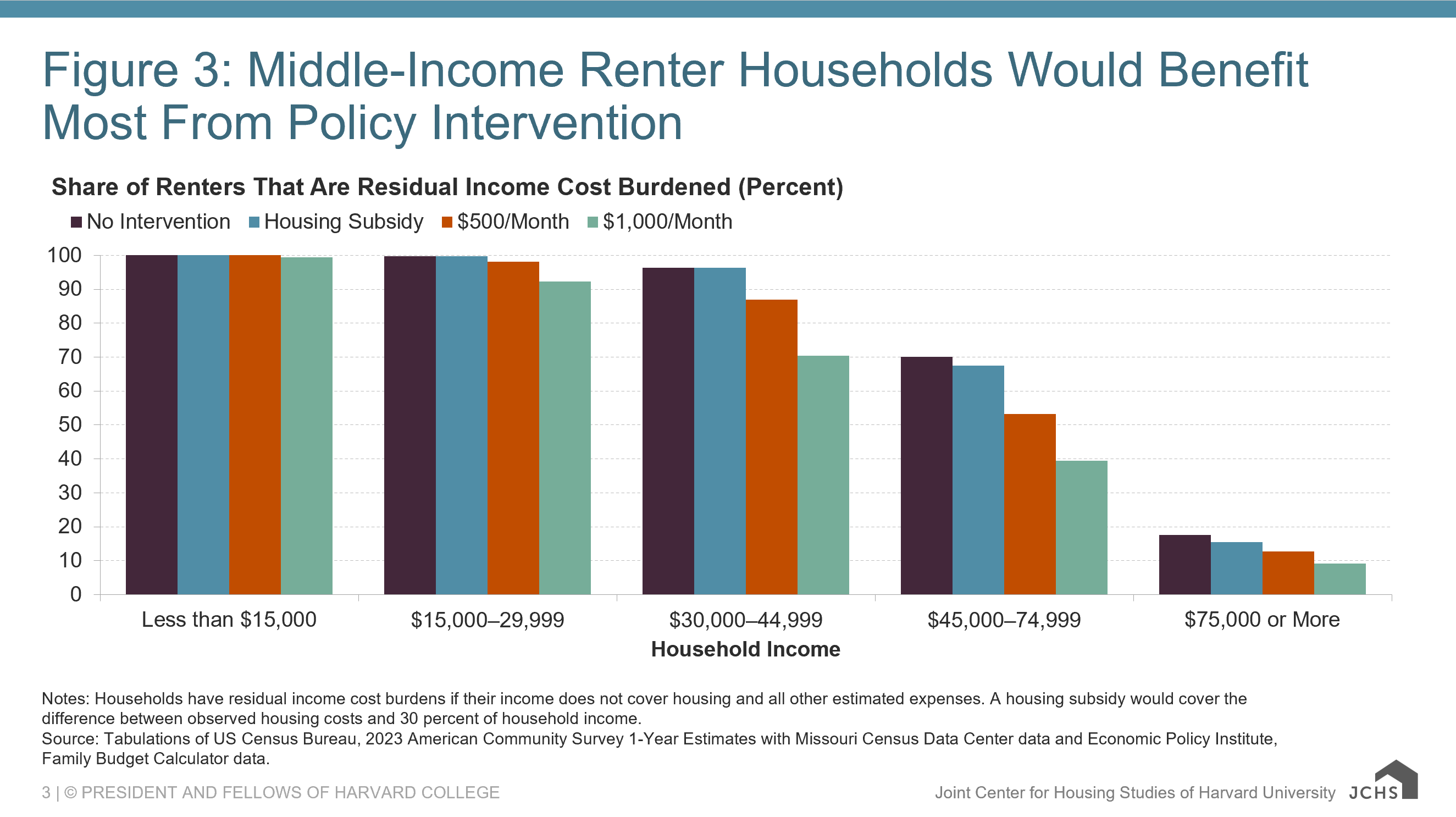

In our paper, we explore three policy interventions to reduce the residual income burden rate for renters: giving all burdened households a subsidy that would cap their rent at 30 percent of income, a $500 per month cash allowance, or a $1,000 per month allowance. A housing subsidy would reduce residual income cost burdens only slightly (1.3 percentage points) but would be the most progressive policy, providing larger amounts to lower-income households than to higher-income households (Figure 3). A flexible $500 allowance would bring rates down by 7.3 percentage points, while doubling that amount would produce a 15.2 percentage point drop. Each of these subsidies would have the greatest effect on reducing the residual income burden rate of middle-income households, who are close to reaching a modest standard of living but have high burdens to begin with.

Figure 3: Middle-Income Renter Households Would Benefit Most from Policy Intervention

Notes: Households have residual income cost burdens if their income does not cover housing and all other estimated expenses. A housing subsidy would cover the difference between observed housing costs and 30 percent of household income.

Source: Tabulations of US Census Bureau, 2023 American Community Survey 1-Year Estimates with Missouri Census Data Center data and Economic Policy Institute, Family Budget Calculator data.

While rent subsidies would free up more income to meet other needs and potentially offer greater residential stability, giving a housing subsidy to every household that is currently burdened would do little to move the needle. Individual policies, like increasing SNAP benefits or offering universal pre-K programs, would similarly have small effects on residual income burdens, a reality we discussed in our earlier paper. These policies are still extremely important, providing crucial relief and benefiting households in many ways, but ultimately, our findings suggest that tinkering at the edges of specific policies does little to address the reality that costs are too high and incomes are too low. Instead of incrementally increasing anti-poverty programs, flexible and generous income supports would enable households to meet the many costs they face and could have the largest impact on reducing renters’ affordability burdens.