The Impact of Student Loan Debt on the Housing Decisions of Young Renters

In the last several presidential debates, both Democratic and Republican candidates have referenced the mounting costs associated with a college education, which have contributed to the dramatic growth in student loan debt over the past decade. Two weeks ago, the nonprofit Institute for College Access and Success released their tenth annual report which showed that students’ average debt at graduation rose 56 percent, from $18,550 in 2004 to $28,950 in 2014. Aggregate outstanding student loan balances more than tripled in real value over the same timeframe, rising from an average of $380 billion in 2004 to $1.1 trillion in 2014, according to data from the Federal Reserve Bank of New York’s Consumer Credit Panel. In fact, student loan debt was the only type of consumer debt to rise steadily during the Great Recession, even as households shed other types of non-housing-related debt such as credit card debt.

Many in the housing industry are concerned that unmanageable student debt is holding back Millenials from becoming first-time homebuyers. Households aged 25 to 34 typically account for just over half of all first-time buyers, but homeownership rates among this group have dropped by more than 9 percentage points since 2004. A 2014 survey conducted by the National Association of Realtors found that only a third of 2014 homebuyers were first-time purchasers—the lowest share since 1987—and that among the 23 percent of first-time homebuyers who reported difficulties with saving for a down payment, over half (57 percent) cited student loans as a factor. In a new research brief I analyze the extent to which young renter households in their 20s and 30s are burdened by their student loan payments and explore the potential implications of these payment burdens on future decisions to pursue homeownership. I also build on the findings described in an earlier blog post to further describe the growth and prevalence of student loan debt among various demographic groups, especially among minority households and those without a four-year college degree.

My analysis draws on cross-sectional data from the Federal Reserve Board’s triennial Survey of Consumer Finances (SCF), which describes changes in debt, wealth, and assets at the household level. My brief utilizes the thresholds for student loan debt burdens outlined by the Consumer Financial Protection Bureau, which define burden according to percentage of monthly income made up by each monthly payment: for low, medium and high burdens, respectively, this percentage is less than 8, between 8 and 14, and more than 14. Reflecting both increases in student loan payment amounts and income declines among young renters, I find that the prevalence of young renters with medium or high student debt burdens accelerated following the Great Recession. Between 2007 and 2013, the share of young renters with high student loan burdens nearly quadrupled, from 5 percent to 19 percent (Figure 1).

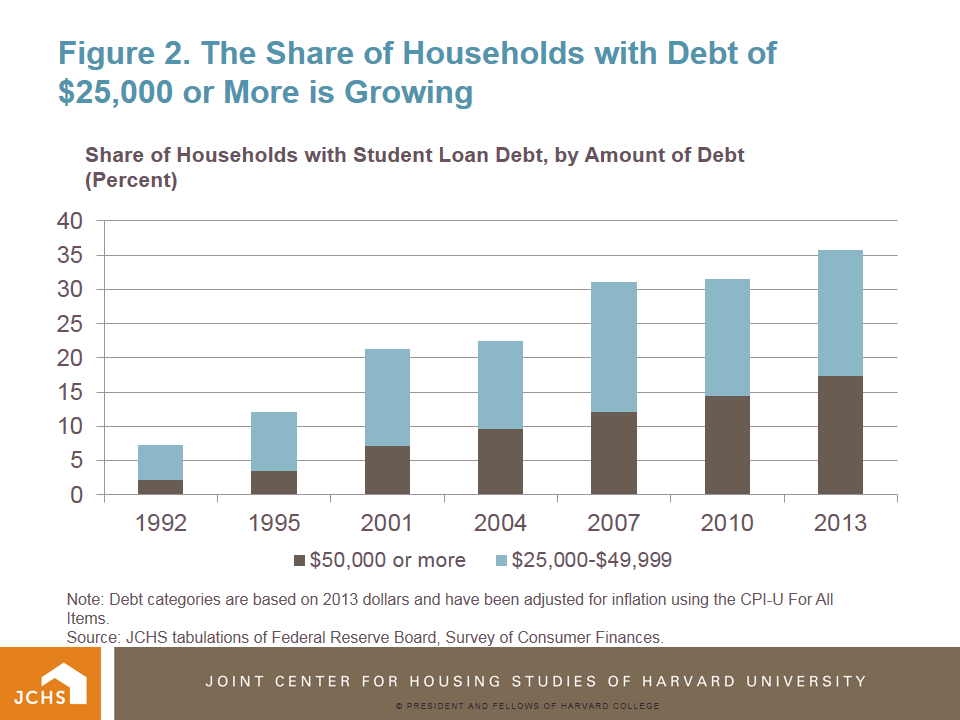

Young renters at the lower end of the income distribution are more likely to bear the brunt of student debt payment burdens. When factoring in other non-housing debt payments on top of student loan payments, the mean payment-to-income ratios increase to 22 percent for young renters in the bottom quartile and to 8 percent for those in the top quartile (Figure 2). Yet although the lowest-income renters are faced with the highest payment burdens, even the lower payment burdens among renters in the top quartile are large enough to be factored into the ability to purchase a home.

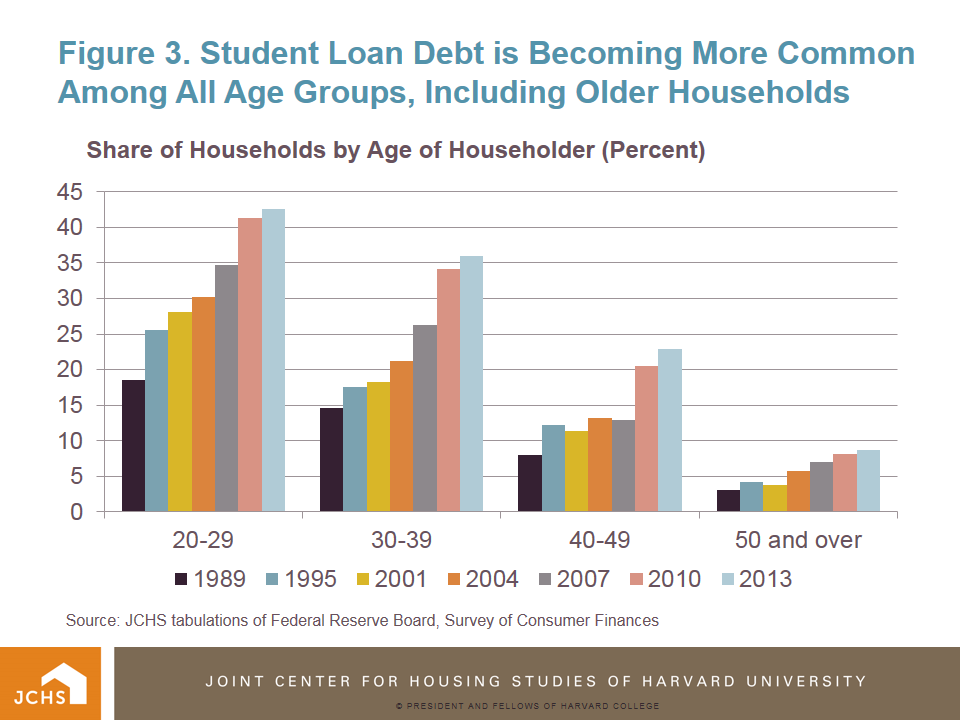

While a causal relationship among student loan debt, housing consumption, and the tenure decisions of young renters cannot be drawn without additional analysis that disentangles other economic factors such as local employment and housing market conditions, student loan payment burdens are likely contributing to downward pressure on the homeownership rates of young households. Indeed, homeownership rates have been consistently lower among households with medium and high payment burdens relative to those with low burdens (Figure 3).

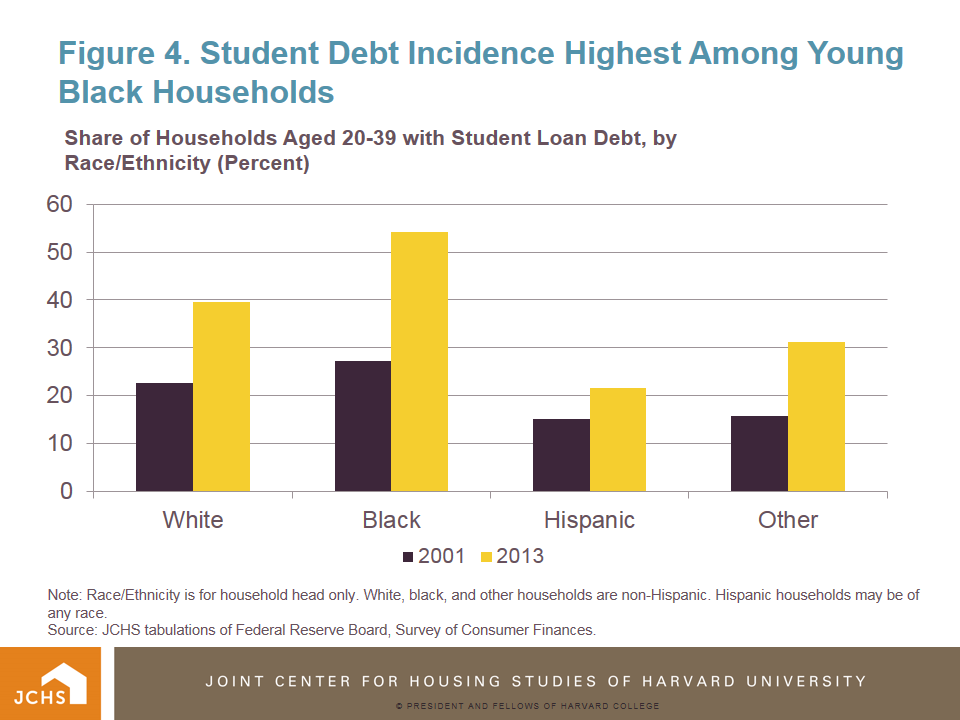

My analysis of student debt burdens excludes households that have not begun making payments on this debt due to deferral or forbearance, suggesting that the number of young renter households with student debt payment burdens is likely to increase in coming years as this group enters the repayment cycle. Indeed, as of 2013, nearly half of the $711 billion in student debt observed in the SCF data was held by households that have at least one student loan in deferral—and 45 percent of renter households aged 20-39 with student loan debt have not yet made any payments toward their outstanding student loan balances (Figure 4).

Another concern is rising student loan default rates, which reflect a growing share of borrowers struggling to pay down their debt. According to the U.S. Department of Education’s Federal Student Aid Data Center, 3.2 million borrowers are in default as of the third quarter of 2015, up by more than half (52 percent) from the same quarter two years ago. Federal student loan borrowers faced with unexpectedly low earnings can take advantage of several income-driven repayment plans that reduce monthly payments and can help minimize payment burdens, but most do not, instead opting for standard repayment plans, not based on current income, where monthly payments are amortized over a 10-year period. Unlike income-driven repayment plans, standard repayment plans do not account for reductions in a borrower’s income and do not establish timelines for forgiveness of any remaining loan balances.

Rising student debt levels and payment burdens among young renters are likely to impact this group’s long-term finances and their decisions to transition to homeownership. Delinquency and default can harm the ability of young renters to access low-cost credit and qualify for a home-purchase mortgage. Furthermore, student loan payments reduce young renters’ discretionary income and can delay the accumulation of savings toward a down payment on a home. Indeed, according to the SCF, college-educated renters in their 20s and 30s with student loan debt had just $3,500 in cash savings and negative net wealth of -$9,640 at the median, compared to $27,000 in net wealth and more than double the amount of cash savings ($7,500) among those without student debt. With lower incomes, wealth, and savings, young renters with student debt may face challenges qualifying for a mortgage to purchase their first home or setting aside a sufficient financial cushion for a down payment on a home.