How Have Renters Responded to Financial Stress in the Pandemic?

Estimates of rent arrearage do not paint a complete picture of the financial toll the pandemic has taken on renters, according to a new paper jointly published by the Center and the Urban Institute, which are both part of a new Housing Crisis Research Collaborative.

For “Renters’ Responses to Financial Stress During the Pandemic,” researchers from our Center and the Urban Institute reviewed available data about the millions of renters who have been especially hard hit by the economic impacts of COVID-19. The research used a variety of surveys, including the Census Bureau’s ongoing Household Pulse Survey.

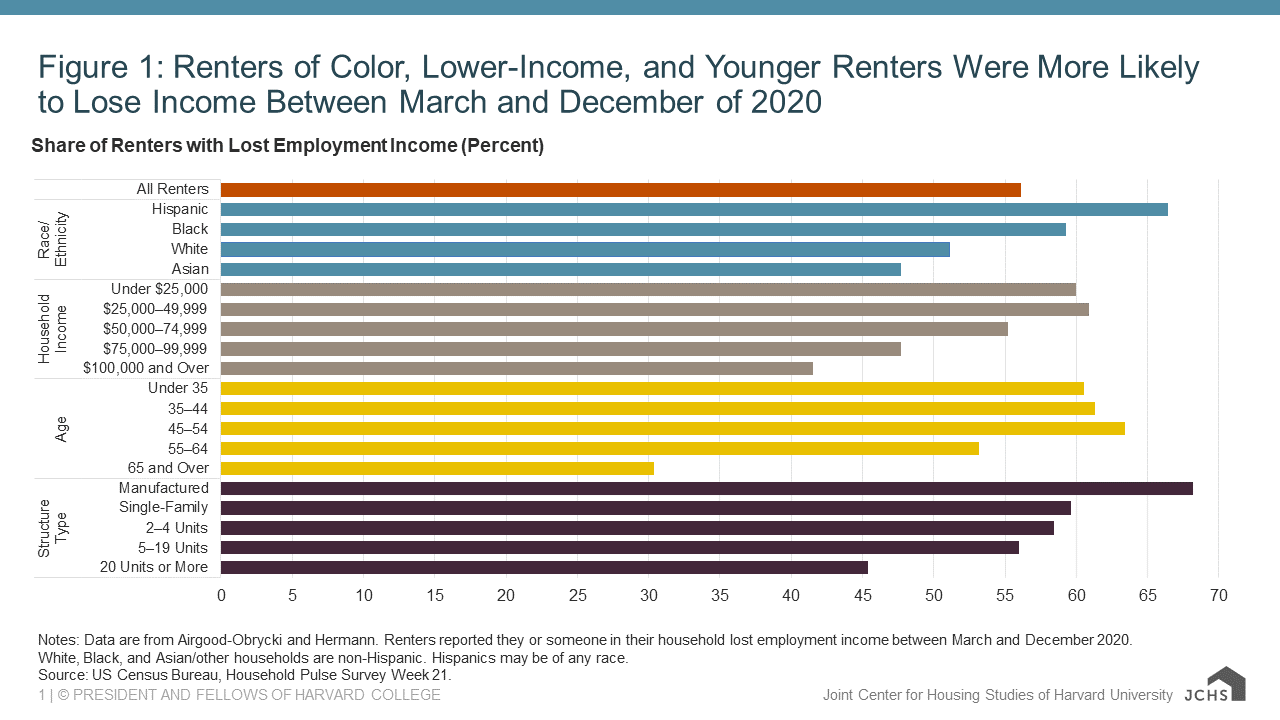

While much of the research to date has produced similar results, some studies have reached different conclusions about the nature and extent of renters’ financial struggles. In our review, we found that many of these differences stemmed from variations in the scope, scale, wording, and timing of the studies and surveys. When these factors are taken into account, most studies indicate that incomes fell for about half of all renters over the last year. Moreover, the losses were larger among renter households headed by people of color, those with lower incomes, and younger people (Figure 1). However, there is limited information about the magnitude of income loss for all renters and for particularly hard hit groups. A few surveys suggest that, early in the pandemic, as many as 40 percent of renters lost at least half of their income; a small recent survey found that, as of early 2021, this share had fallen to about 25 percent of all renters.

Figure 1: Renters of Color, Lower-Income, and Younger Renters Were More Likely to Lose Income Between March and December of 2020

Notes: Data are from Airgood-Obrycki and Hermann. Renters reported they or someone in their household lost employment income between March and December 2020. White, Black, and Asian/other households are non-Hispanic. Hispanics may be of any race.

Source: US Census Bureau, Household Pulse Survey Week 21.

Renters responded to these losses in a variety of ways. Many tapped their savings, though the estimates of who did so ranged from 25 to 40 percent of renters. Some information also suggests that a quarter of renters have substantially depleted their savings since the beginning of the pandemic. Borrowing from family and friends was another means of coping with income loss, with about 25 percent of all renters turning to this option including about half of renters who were behind on rent. And while estimates vary, most surveys found that 5 to 15 percent of renters were able to secure reduced rent payments from their landlords, at least temporarily. Several studies also found that about 30 percent of renters relied on government support–such as unemployment insurance or stimulus payments—to pay rent at some point during the pandemic, although only 2 to 3 percent of renters were able to tap smaller emergency rent assistance programs that were part of early pandemic relief efforts in 2020.

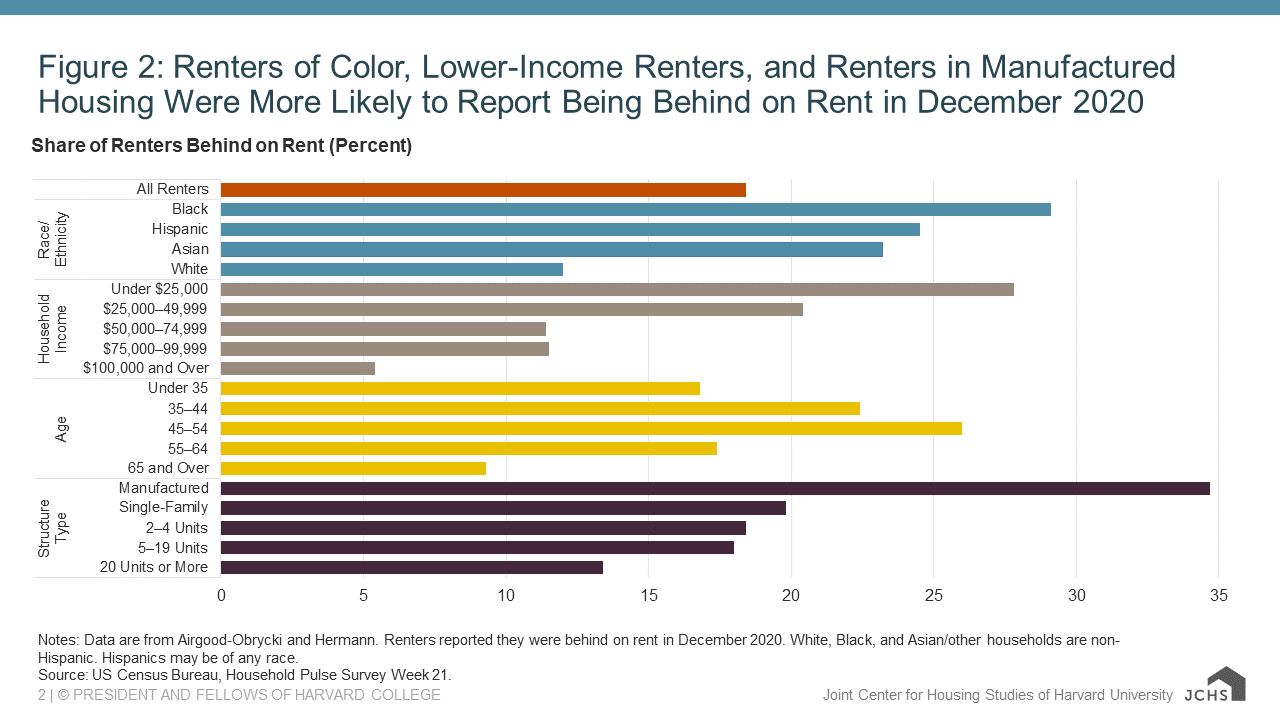

Despite these efforts, studies indicate that between 10 to 20 percent of renters were behind on rent at the end of 2020 or the beginning of 2021 and that those hardest hit by the pandemic–renters of color, low-income renters, and middle-aged renters–were more likely to be behind on their rent (Figure 2). Estimates of the total amount of back rent owed vary: several studies estimate renters typically owed $1,000-2,000, while others put the average at $5,000-6,000. In addition, a few small studies have indicated that those behind on rent have been more likely to suffer from food insecurity and/or have health problems.

Figure 2: Renters of Color, Lower-Income Renters, and Renters in Manufactured Housing Were More Likely to Report Being Behind on Rent in December 2020

Notes: Data are from Airgood-Obrycki and Hermann. Renters reported they were behind on rent in December 2020. White, Black, and Asian/other households are non-Hispanic. Hispanics may be of any race.

Source: US Census Bureau, Household Pulse Survey Week 21.

This research has important implications for the design and implementation of federal COVID-relief programs and for future efforts to help renters. Notably, the research shows that cash assistance in a variety of forms—not just the infusion of rent relief from the recent CARES Act but also from unemployment insurance, stimulus checks, SNAP, and subsidies for health insurance—have been and will continue to be critical. This, in turn makes it clear that programs to aid renters need to consider a household’s full financial picture–depleted savings accounts, loans taken out to cover the rent and other costs, and reduced spending on essentials—in determining eligibility and level of assistance.

Policymakers should also streamline screening for rental assistance programs and lift barriers to accessing aid. In addition, rental assistance programs should be designed to help close racial equity gaps while complying with fair housing laws. Finally, policymakers should invest in more and better data on renters’ financial health and eviction risk. Taken together, these steps can not only help alleviate the problems created for renters by the pandemic, but address many of the longstanding inequities that have become more evident over the last year.