Great Recession Increased Fragmentation in Remodeling Industry

During the last industry downturn, home remodeling contractors experienced increased fragmentation due to especially large growth in small and self-employed remodelers. Additionally, concentration gains that were achieved by larger-scale firms in the industry upturn were reversed somewhat—all according to recently acquired tabulations of the U.S. Census Bureau’s 2012 Economic Census and Nonemployer Statistics. Conducted once every five years, the Economic Census measures payroll business activity at the industry level, while the Nonemployer Statistics capture similar data for businesses with no paid employees. Special tabulations of the Economic Census and Nonemployer Statistics done for the Joint Center’s Remodeling Futures Program specifically isolate residential construction businesses—either general (i.e. full-service and design/build) or special trade (e.g. HVAC/plumbing, electrical, painting, and roofing)—who have more than half of receipts from remodeling and repair activity.

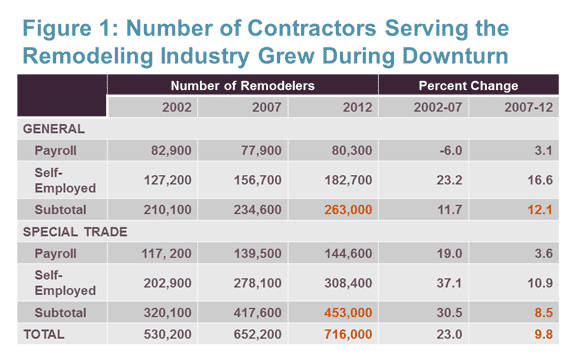

According to Joint Center estimates from these data sources, the number of residential remodeling contractors reached 716,000 by 2012, up from 652,000 at the peak of the market in 2007 (Figure 1). General remodelers increased their ranks over 12% to 263,000, and special trade remodelers increased 8.5% to 450,000. Overall, the total number of contractors serving the remodeling industry increased almost 10% from 2007. Most of this growth, however, was driven by increases in self-employed remodelers, who saw double digit growth between 2007 and 2012—about 11% for special trades and nearly 17% for general remodelers. The number of payroll contractors grew only 3.5% during this same period.

Sources: JCHS estimates using unpublished tabulations from US Census Bureau, Economic Censuses of Construction and Nonemployer Statistics.

The self-employed already made up a large share of home improvement businesses before the boom and bust—about 62% in 2002—and by 2012 their share increased to almost 70% of businesses operating in the remodeling industry. Of course, even though self-employed contractors are a growing share of remodeling businesses, they remain very small businesses: 44% had receipts less than $50,000 in 2012 and 29% had receipts between $50,000 and $99,999. Although the number of self-employed remodelers with less than $150,000 in annual receipts* increased 15% from 2007-2012, those with receipts of $150,000 or greater increased only 3%. Indeed, much of the increased fragmentation in remodeling contractors occurred at the smallest end of the revenue spectrum.

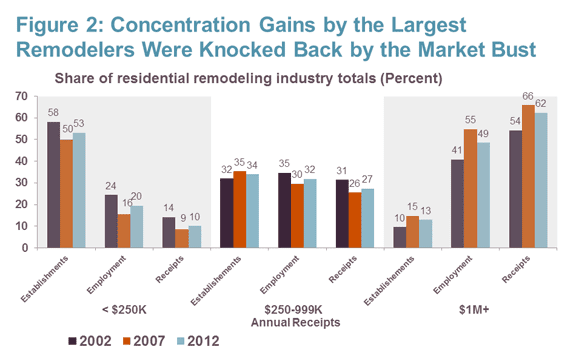

Even remodeling contractors with payrolls continue to be dominated by smaller-scale businesses: over half of payroll remodelers generated under $250,000 in revenue in 2012 (Figure 2). However these smaller-scale remodelers only accounted for 10% of total payroll receipts. Larger-scale firms with $1 million or more in revenues made up just 13% of all remodeling payroll businesses in 2012 but were responsible for generating 62% of total industry receipts and accounting for nearly half of industry payroll employees. Although these largest remodeling firms saw a decline in their shares of industry establishments, employment, and receipts from the peak of the market in 2007, they remained well above pre-boom shares of a decade ago in 2002. Even after suffering the worst market declines on record, larger-scale remodeling companies continue to play a dominant role in the market.

Source: JCHS tabulations of unpublished data from US Census Bureau’s Economic Censuses of Construction.

In fact, when considering the very largest general remodeling companies in terms of value of receipts over the 2002 to 2012 period, the largest 50 firms continued to increase their share of industry receipts. In 2002, the 50 largest remodelers accounted for 5% of all industry receipts generated by general remodelers with payrolls. This share jumped to 7.9% by 2007 as the market boomed, but even during the industry collapse, the top remodelers were still able to increase their market share to 8.5% of total receipts. The average value of residential remodeling receipts for the top 50 general remodelers with payrolls was over $85 million in 2012, which at first might sound unrealistically high given that the average general remodeling firm had under $650,000 in revenue that year, but could be explained with even just one significant outlier skewing the concentration figures.

Ultimately, these recent data releases provide important updates on the evolving structure of the remodeling contracting industry and a more complete understanding of the impact of the Great Recession. The remodeling industry experienced increased fragmentation during the market downturn, especially among smaller contractors. Larger-scale firms did lose some of their concentration gains of the boom years, but there is evidence that the remodeling industry continued to concentrate at the very top of the market. The top 50 largest companies increased their share of industry receipts even during the downturn, a considerable advantage of scale. Further analysis of the changing composition and organization of remodeling contracting firms over the past business cycle will be included in a research note to be published later this year.

*receipt categories not adjusted for inflation