Are More Older Americans Retiring with Mortgage Debt?

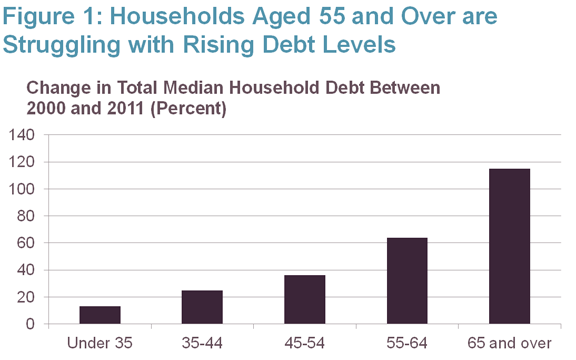

As the first wave of baby boomers prepare for retirement, it would be easy to assume that they’ve paid off their mortgage and credit card debt. However, data from the Census Bureau’s Survey of Income and Program Participation (SIPP) shows that older Americans today are grappling with mounting debt levels, even into their retirement years. Among households aged 55 to 64, total median household debt jumped from $42,654 in 2000 to $70,000 in 2011—a 64 percent increase—while households aged 65 and over are now carrying more than twice the amount of household debt they were carrying a decade ago. Even more surprisingly, older Americans had a larger increase in total median household debt than younger households, with the amount of total median household debt among householders under the age of 35 growing by a relatively modest 13 percent between 2000 and 2011.

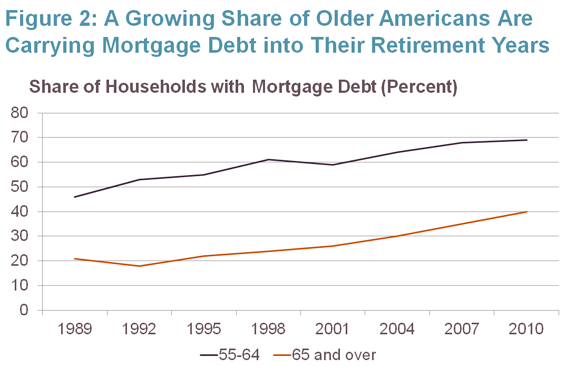

The increase in debt among older Americans has been driven by a spike in the number of households who hold secured debt, which includes mortgages and home equity loans, even into their retirement years. According to data from the Survey of Consumer Finances, the share of households aged 65 and over with mortgage debt has nearly doubled over the past 20 years, from 21 percent in 1989 to 40 percent in 2010; among households aged 55-64 during the same time period, the share grew from 46 percent of households in 1989 to 69 percent in 2010. Just between 2001 and 2010, there was a 10 percent increase in the share of households aged 55-64 with mortgage debt and a 14 percent increase in the share of households aged 65 and over with mortgage debt.

It’s not just that more seniors are carrying mortgage debt; they are also saddled with much higher mortgage debt than they were carrying 20 years ago. Although the median mortgage debt of all homeowners who are still carrying mortgage debt has increased from nearly $54,000 in 1989 to $109,000 in 2010, among homeowners aged 65 and over there was a 76 percent increase in the median amount of mortgage debt, from $15,180 in 1989 to $63,000 in 2010 (after adjusting to 2010 dollars).

While the dramatic rise in the share of older Americans with mortgage debt is partly the result of easily-accessible credit before the Great Recession (when many Americans took out home equity loans, extended mortgage terms, or refinanced their homes and took out cash), there is also evidence that older households were not spared from the Great Recession. A 2011 AARP study points out that, post-recession, a larger share of older homeowners with mortgages, particularly those with incomes below $23,000, are paying 30 percent or more of their income for housing costs. In fact, 96 percent of homeowners aged 50 and older with mortgages, who have incomes under $23,000, pay 30 percent or more of their income for housing.

Furthermore, a recent report from the Consumer Financial Protection Bureau (CFPB) indicates that more senior households are taking out reverse mortgages. According to the report, 70 percent of reverse mortgage borrowers in 2010 opted to take the full amount of the loan as a lump sum at closing, up from just 2 percent of borrowers in 2008. While data is not available on how they use these funds, this dramatic increase raises concerns about whether borrowers will have sufficient financial resources to cover their expenses later in life.