What Impact Do Changing Interest Rates Have on Mortgage Demand?

Could the post-Great Recession drop in housing demand have been driven in part by an increase in mortgage credit spreads across borrowers? In a new Joint Center working paper that uses proprietary data on the spread of mortgage rates across borrowers with different credit, I find that mortgage demand does react to mortgage interest rates in economically and statistically significant ways.

This finding is significant because little is known about the extent to which changes in interest rates affect the demand for mortgages. Measuring this effect is difficult because both interest rates and the demand for mortgages are driven by macroeconomic factors. For example, after the financial crisis in the late 2000s, interest rates fell as the Federal Reserve attempted to stimulate the economy, but the demand for mortgages also fell because individuals faced adverse macroeconomic conditions. A naive estimate would suggest that over this period, lower interest rates drove lower housing demand, which is clearly not correct.

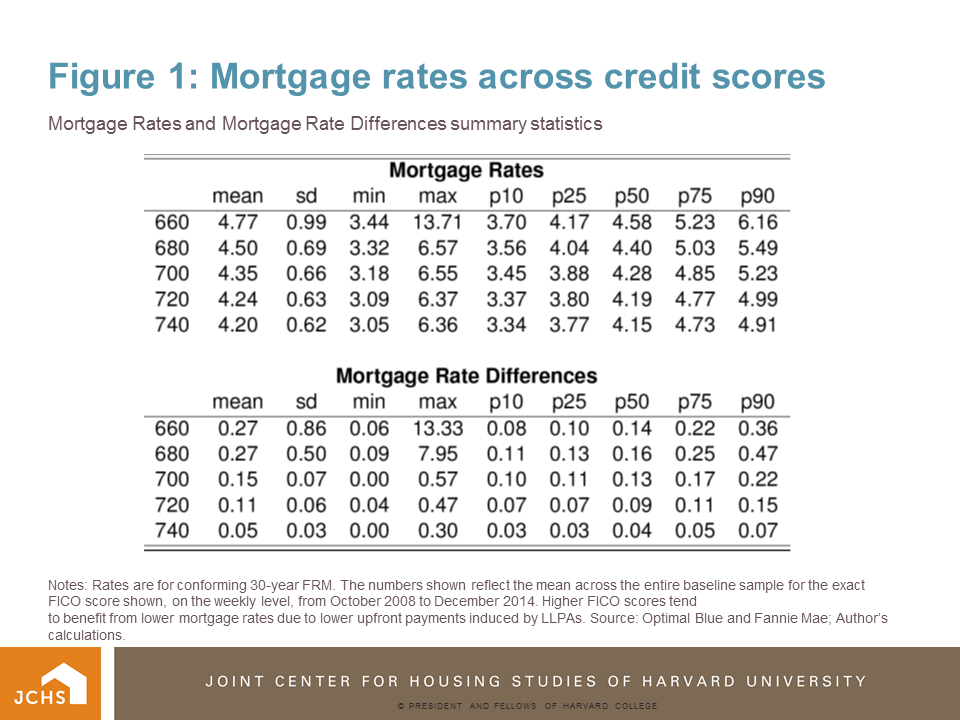

My study uses Loan Level Price Adjustments (LLPAs) to address this issue. Instituted by FHFA in November 2007, LLPAs are additional fees paid upfront by the lender to Fannie Mae or Freddie Mac. The fees are higher for loans with higher loan-to-value ratios and borrowers with lower credit scores, and feature discrete cutoffs at certain credit scores, as measured at mortgage origination. Put simply, a borrower with a 700 credit score will face the same LLPA as a borrower with a 701 credit score, but will benefit from a discretely lower LLPA than a borrower with a 699 credit score.

Using administrative mortgage rate data, I find that LLPAs are completely passed through to borrowers, so while lenders receive the same mortgage rate across credit scores, borrowers just below a credit-score cutoff pay a higher mortgage rate than those just above that cutoff point (Figure 1). I further show that borrowers across these credit scores are virtually identical, and for high credit scores, lenders do not differentially screen across these cutoffs. This allows me to apply a regression-discontinuity design to examine how mortgage demand changes for borrowers just above and below several credit score cutoff points—660, 680, 700, and 720—where the interest rates offered to borrowers change.

Source: Optimal Blue and Fannie Mae; Author’s calculations.

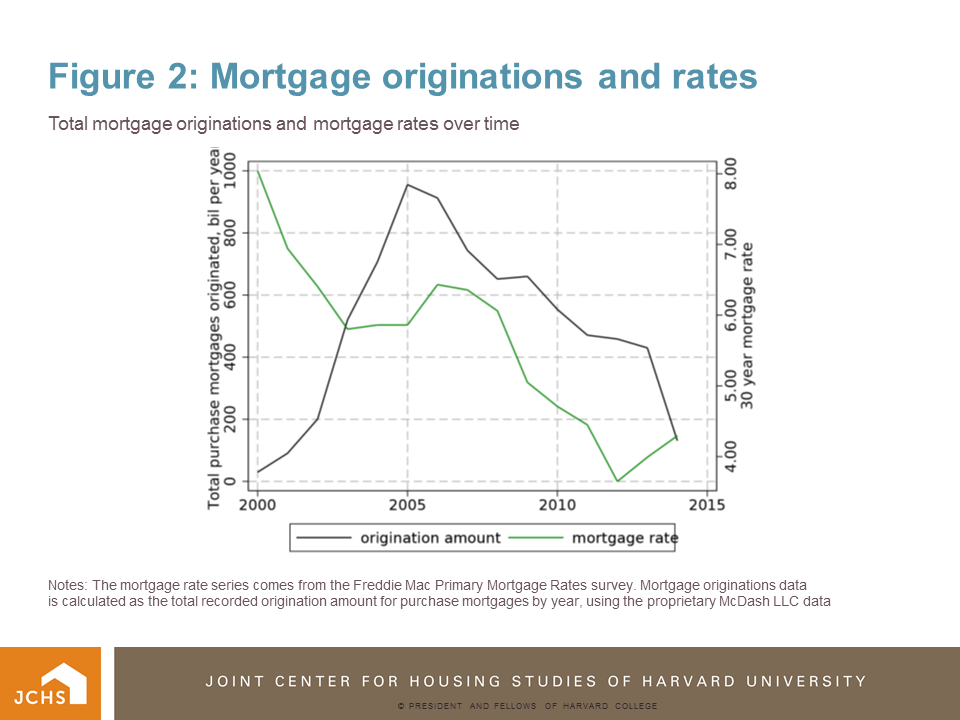

The results show that borrowers respond to changes in interest rates in economically and statistically significant ways (Figure 2). I estimate that a 25 basis point cut in interest rates results in a 50 percent increase in the likelihood of a potential borrower to demand a loan. In a given month, this increases the number of mortgage originations from about 100 per 100,000 individuals to 140 per 100,000 individuals. I also find that a 25 percent basis point cut in interest rates results in an increase in loan size of approximately $15,000, or about 10 percent of the average origination volume.

These estimates help to explain the post-crisis drop in mortgage demand from low-income and low-credit borrowers. A back-of-the-envelope calculation using my estimates suggests that, had 680-719 FICO borrowers been subject to the same LLPA as 720 FICO borrowers, this group would have generated $15 billion more in mortgage demand over six years, which would have been a 33 percent increase in mortgage lending to this group alone. More generally, my estimates suggest that borrowers were very sensitive to mortgage rates after the crisis, implying that the Federal Reserve’s efforts to lower interest rates, which in turn lowered mortgage rates, may have been very effective in bolstering the housing market.