Making Apartments More Affordable Starts with Understanding the Costs of Building Them

This piece is the first in a four-part series on innovations in design and construction co-published with The Brookings Institution. It summarizes findings from a report written by Hannah Hoyt, published by Harvard’s Joint Center for Housing Studies and NeighborWorks America.

During the decade between the Great Recession and the coronavirus pandemic, the US experienced a historically long economic expansion. Demand for rental housing grew steadily over those years, driven by demographic trends and a strong labor market. Yet the supply of new rental housing did not keep up with demand, leading to rent increases that outstripped gains in household income.

Policymakers and researchers have identified a number of barriers to building more—and more affordable—housing, including restrictive land use regulations, increasing costs of construction labor and materials, and greater market concentration in the homebuilding industry. Notably, residential construction has not benefited from improved productivity, as many other industries have.

Construction will likely slow down until the COVID-19 pandemic abates and economic conditions improve. But the public health crisis has highlighted the extent of housing insecurity among millions of US renters—a problem that can only be solved by building more housing at lower costs.

This piece is the first in a series that explores how improved design and construction decisions could reduce the cost of building multifamily housing. Our goal is to lay out what developers, architects, and contractors can do to improve affordability, independent of larger changes in land use policy or housing finance. We also note areas where design and construction interact with the policy and finance environment, and which would benefit from broader changes. The series summarizes key findings from a longer report.

Demand for rental housing has outstripped supply—especially for moderately priced apartments

Between 2010 and 2019, the share of US households that rent their homes rose from 32 percent to 36 percent. Over 4 million new renter households were formed during that period, including an unprecedented increase in high-income renters. This surge in demand led to historically low rental vacancy rates and rents rising faster than household incomes. Low- and moderate-income renters were especially squeezed as higher-income households competed for limited rental supply. Household size declined over this period, translating into increased demand for small housing units, especially one- and two-bedroom apartments.

On the supply side, apartment buildings were growing larger (Figure 1). Over 60 percent of new multifamily units completed in 2018 were in buildings with more than 50 units, while only 5 percent were in buildings with under 10 units.

Larger buildings reflect economies of scale in multifamily construction. As land costs increase, developers need to fit more housing units on a single land parcel. The costs of design, regulation, and operations don’t vary much by building size, so larger buildings allow developers to spread these fixed costs over more apartments. As one developer put it: “From an operations standpoint, it costs almost as much for us to operate a 30-40 unit building as it does a 100-unit building, so we are looking for sites that can accommodate larger projects.”

Figure 1: Share of multifamily units completed by building size, 2000 to 2018

Source: US Census Bureau Survey of Construction.

Rising rents between 2010 and 2018 reflect substantial cost increases in the three major components of construction: land, labor, and materials. Local and state governments have adopted regulations—including impact fees and complex permitting processes—that increase development costs and extend construction timelines. Local zoning laws are much more restrictive of new multifamily housing than single-family housing in nearly every jurisdiction across the US.

When governments add costs to development, these costs typically get passed on to renters or buyers with a markup. Onerous regulations can impose a significant burden, especially on smaller-scale projects and affordable or middle-income housing.

While academic literature has documented how overly restrictive zoning increases housing costs during early stages of the development process, less research has focused on the housing design and construction phases. To date, most design and construction research on housing costs focuses on individual construction techniques (such as off-site construction) or specific building types (such as micro-units). Project teams will need to combine a range of established and experimental strategies to increase the efficiency and predictability of multifamily design and construction while producing high-quality housing.

Reducing construction costs will require savings at all stages of the process

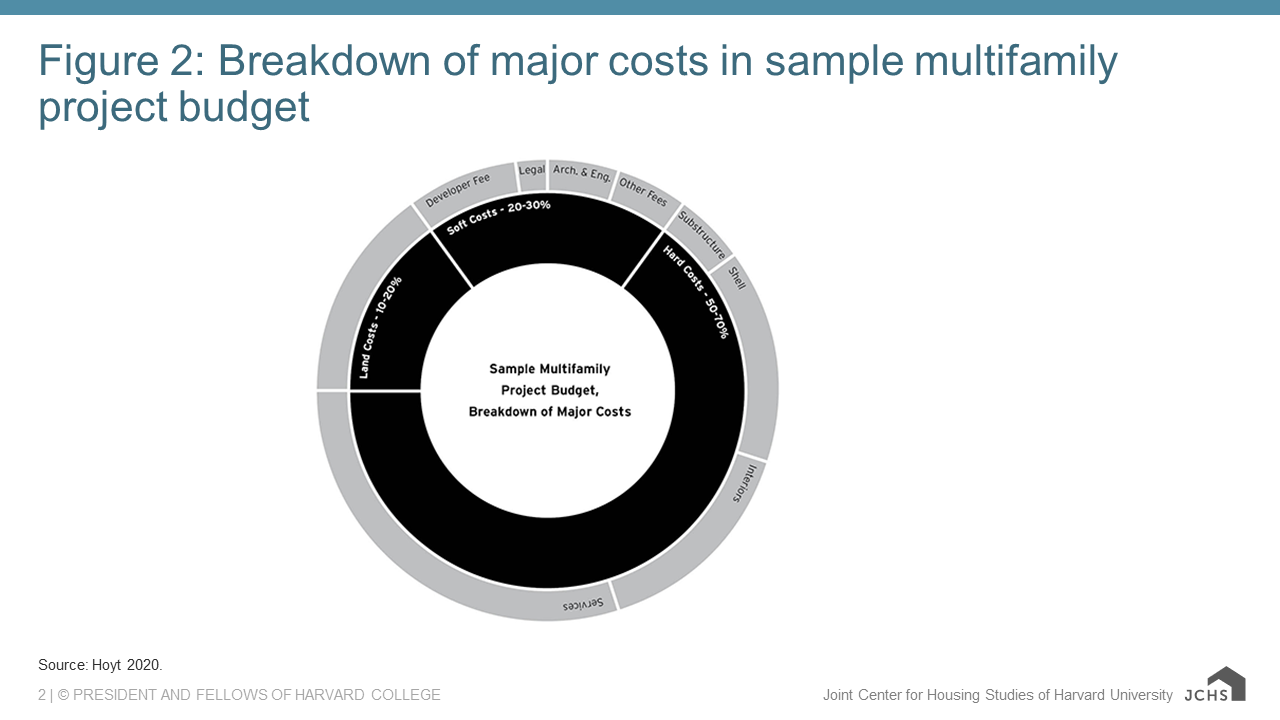

To better understand how design and construction techniques can make building apartments cheaper, we break down the component costs into three categories: land costs, hard costs, and soft costs. How much each category contributes to total development costs varies substantially based on geography, project type (e.g., mid-rise versus high-rise), project size, and specific site characteristics. The following breakdown approximates how major costs might be divided in a mid-rise (four- to six-story) multifamily project.

- Land costs. Purchasing land accounts for roughly 10 percent to 20 percent of total development costs for a typical multifamily project. Land values vary substantially based on project location. As of 2018, land prices near downtown Washington, D.C. and San Francisco were well over $10 million per acre, compared to around $100,000 per acre in Cleveland and Detroit.

- Hard costs. This category includes construction labor and materials, and can be broken down into four subcategories: site prep and substructure, shell and structure, interiors, and services. On average, hard costs account for 50 percent to 70 percent of construction costs.

- Soft costs. All costs besides land and hard costs are designated as soft costs. Key components include design, engineering, financing, permitting, and impact fees. Soft costs average around 20 percent to 30 percent of total costs for a relatively straightforward project, though they can be higher in some metro areas and for subsidized affordable housing projects. Complex projects that require rezoning or that face substantial community opposition will have much higher soft costs.

Later articles in this series will delve into strategies to reduce costs in each of the major categories and subcategories.

Figure 2: Breakdown of major costs in sample multifamily project budget

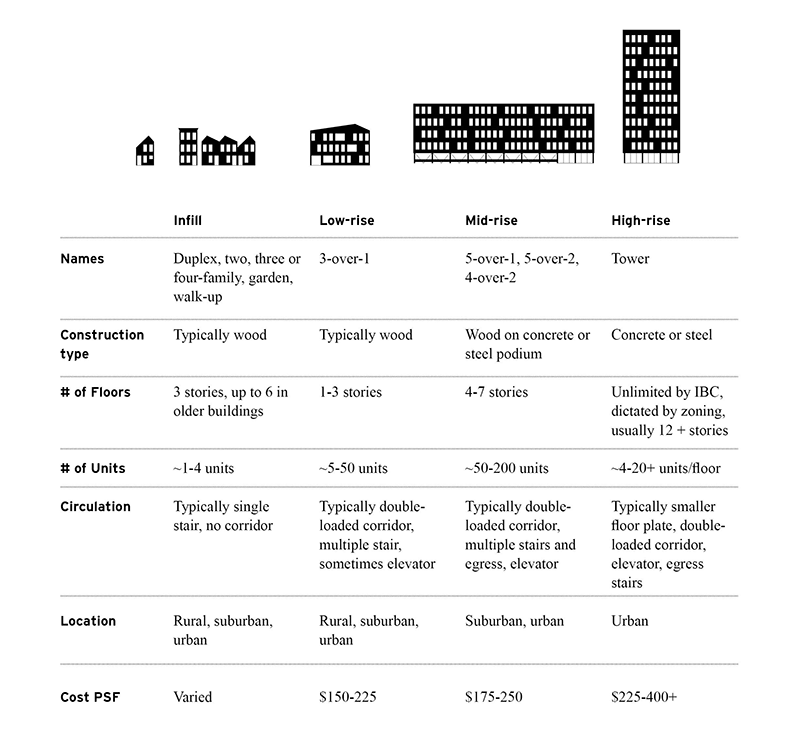

Not all multifamily buildings are skyscrapers—building typologies matter for costs

For many, the term “apartment building” conjures images of glass-and-steel Manhattan skyscrapers. But in reality, multifamily buildings span a range of sizes, architectural styles, and building materials—everything from modest duplexes to courtyard clusters to 50-story towers. Regulations such as building codes and zoning requirements strongly influence building size, design, materials, and construction techniques. Banks and other lenders tie financing availability to building size and structure type as well. All of these factors translate into different per-unit construction costs.

Figure 3: Multifamily housing typology

Construction costs for any given typology can vary significantly across geographic markets, based on prevailing wage rates for construction workers, requirements to hire unionized workers, and building codes. Construction materials such as lumber and steel are subject to global markets, so prices vary less across local areas in the US. The COVID-19 crisis may disrupt global supply chains for these materials.

We present average costs derived from RSMeans data and interviews with developers. However, construction costs must be understood locally. For example, many stick-built, mid-rise projects in Detroit are stalled as labor shortages and strict local labor requirements drive construction costs above $250 per square foot without corresponding increases in rents. Cost estimates in Detroit have become hard to predict, with developers seeing increases of 30 percent between initial cost estimating and final construction bids.

One important caveat is that RSMeans primarily collects data from greenfields projects, not redevelopment projects in infill locations. Infill projects are generally smaller, lack economies of scale, and often occur on more complicated sites. Costs are likely to vary significantly across infill projects, but are likely most similar to mid-rise construction.

Figure 4: Wood frame over concrete is typical for mid-rise apartment buildings

Image Credit: Mid-rise construction in Seattle, 2015. Source: SounderBruce / Creative Commons license via Flickr.

As Figure 3 shows, construction costs change substantially depending on the building type, largely because of the change in materials. For example, a high-rise concrete structure might cost $75 or more per square foot than a six-story wood-frame (“stick”) structure on a concrete podium. If the site is zoned for a maximum building height of nine stories, the additional three stories of revenue generated by switching to the concrete structure may not be sufficient for the deal to “pencil out” (make sense financially). Because of the jump in construction costs, developers may not build to the maximum height or floor-to-area ratio (FAR) allowed under zoning, except in locations where expected rents per square foot are very high.

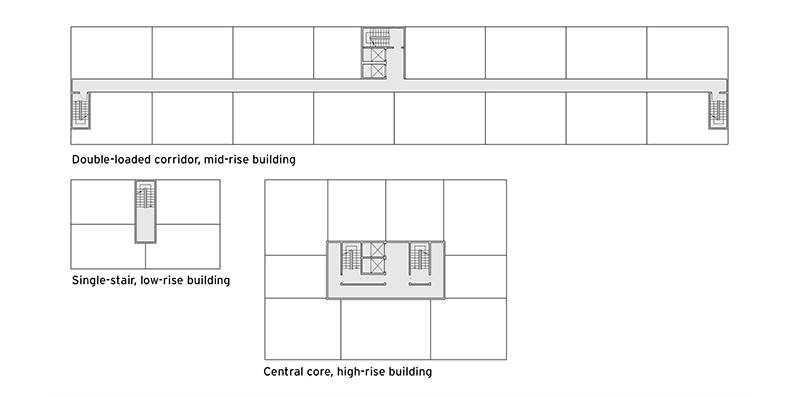

Construction type also influences the layout and efficiency of multifamily buildings, specifically how residents access their individual apartments. Small infill projects often have a single, interior staircase rising from a common entranceway. Mid-rise buildings typically rely on double-loaded corridors with one or more elevators, as illustrated in Figure 5. High-rise towers often cluster apartments around a central core. As we discuss, these layouts have direct cost implications: Taller multifamily towers require more expensive steel or concrete structures, and floor layouts affect the percent of total built square footage that directly generates revenue (e.g., no single resident pays the cost of hallways or stairs).

Figure 5: Construction type influences unit layout and building circulation

So far, our discussion has focused on costs to build market-rate apartments. “Affordable” multifamily buildings (i.e., projects that receive government subsidies) have additional features and constraints that generally increase development costs relative to market-rate housing. Notably, the soft costs of affordable housing are substantially higher because of the complexity of assembling subsidy programs. Affordable housing developers can’t compete for the most desirable land parcels, so they are often limited to sites with lower absolute land costs. These sites may cost less because of the challenges of building on them; for example, steep sites that require more expensive foundations or contaminated land that requires remediation.

States allocating federal subsidies such as the Low-Income Housing Tax Credit (LIHTC) have requirements on unit types and minimum unit sizes (to include larger “family-sized” apartments), which may limit innovation at the floorplan and unit level. Nonprofit developers are often trying to support important community objectives, such as building with union labor, paying prevailing wages, and including community spaces within their housing developments. These efforts, however, can add challenging costs to project budgets.

Searching for savings in every corner of construction

The remaining articles in this series will investigate how better design and construction decisions could bring down the cost of new multifamily housing. While design and construction strategies are no substitute for policy changes at both the federal and local levels, they reflect the reality that project teams across the country face budget gaps and often turn to design and construction to control costs.

Some of the key questions to be addressed include:

- Which categories of costs are largest? Which costs are hardest to predict, or most variable across projects?

- Which costs does the project team control (rather than external partners or government agencies)?

- How could better design and construction reduce costs at each stage of the process?

- How could cost savings be allocated, either through improved quality or passed along to tenants?

Improving housing affordability is critical to reducing financial stress on renter households. It will take cooperation among all partners in the development process—architects, developers, builders, and policymakers at all levels of government—to achieve success.