Institutions and Geographic Concentration in VA Mortgage Lending

The Veteran’s Administration (VA) home loan program, which makes homeownership more affordable for veterans, is used more extensively in places closer to major military installations, according to our new working paper. However, we also find that that utilization of the VA home loan program was lower than one would expect in higher-cost places.

In Institutions and Geographic Concentration in VA Mortgage Lending, we examine the geographic distribution of the VA loan program, which helps make homeownership more affordable to veterans by removing the need for a 20 percent down-payment, without the requirement of private mortgage insurance. Since its inception in the post-WWII era the program has been effective at making homeownership achievable for veterans. Research by others has shown that the VA home loan program increased homeownership rates by lowering the age at which veterans could afford to buy their first home.

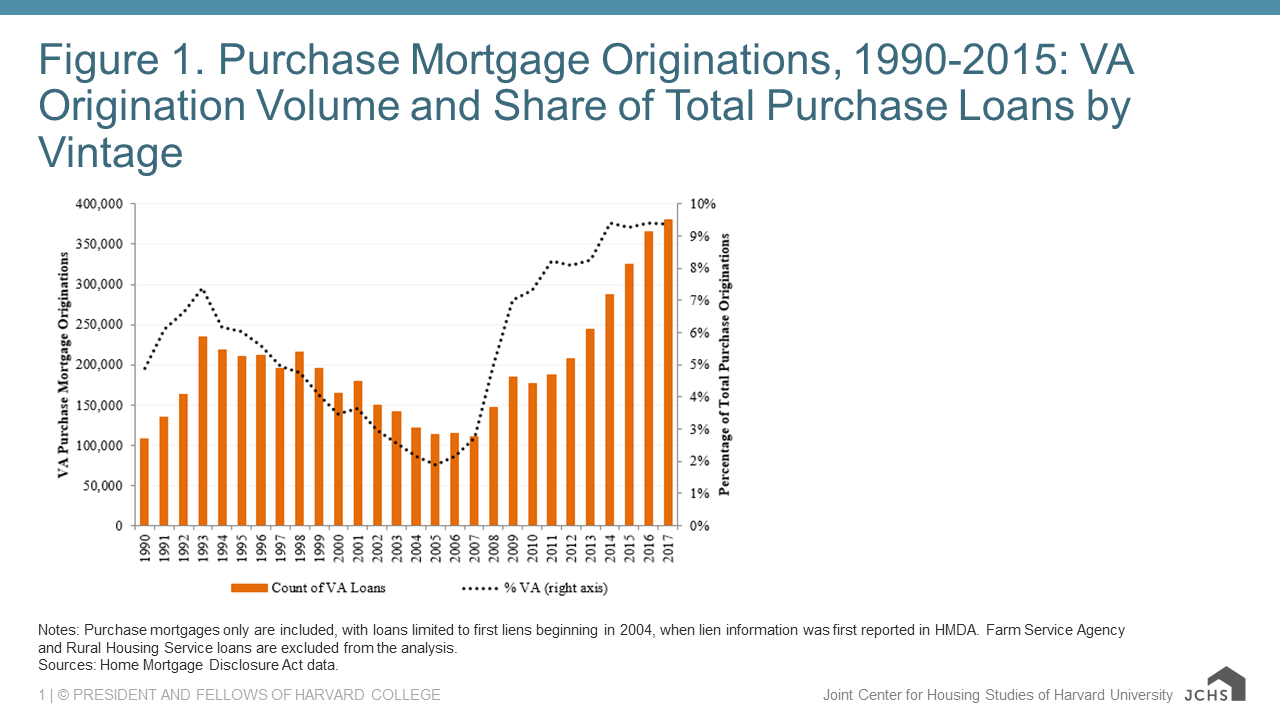

During the housing boom of the nineties and early aughts, the popularity of the program waned, but during the recession and in recent years its popularity has increased, both in real terms and as a share of all mortgage originations. According to Home Mortgage Disclosure Act (HMDA) data, each year since 1990, between 125,000 and 380,000 VA purchase mortgages have been originated. As a percentage of all VA, conventional, and FHA mortgages, VA mortgage originations tend to be counter-cyclical. VA lending made up just 1.9 percent of purchase mortgages at the market’s height in 2005 with 113,000 loans, but as conventional lending shrunk in the housing market recovery, VA lending increased dramatically—both in levels and as a percentage of all lending (Figure 1). By 2017, VA loans made up 9.4 percent of all mortgages, with 380,000 originations—over 3 times the 2005-2007 annual volume and the highest number of VA purchase originations since HMDA data collection began.

Figure 1: Purchase Mortgage Originations, 1990-2015: VA Origination Volume and Share of Total Purchase Loans by Vintage

Source: Home Mortgage Disclosure Act data. Note: Purchase mortgages only are included, with loans limited to first liens beginning in 2004, when lien information was first reported in HMDA. Farm Service Agency and Rural Housing Service loans are excluded from the analysis.

We wanted to understand why some areas of the country have many more VA home loans than others. Outside of the obvious factors of housing costs and the size of the eligible population, we hypothesized that institutions that serve veterans may play a role in increasing utilization of the program. We created a panel data set of 657 counties throughout the US from 2006 through 2017. We combined HMDA mortgage origination data, American Community Survey data, Zillow house price index data, and spatial locations of Veteran Service Organizations (e.g. American Legion), VA facilities (hospitals, clinics, veteran centers, and cemeteries), and Department of Defense installations (i.e. military bases).

We then tested whether proximity to these institutions helped to explain variation in the rates (number of VA loans originated per 10,000 eligible residents) and percentage of all purchase loans originated in a county that are VA mortgages. We found that proximity to a military installation was associated with higher percentages and rates of VA home loan originations. This finding of a positive relationship between VA borrowing and proximity to DOD installations was robust and could not be explained by the share of the population that is eligible to participate, the relative economic status of veterans to nonveterans, area house prices, or the level of demand for general low-down payment lending in the area (as evidenced by FHA borrowing). The robustness of our results supports the hypothesis that proximity to military institutions (particularly bases) matters, and may help influence VA lending patterns. One possibility is that lenders, real estate brokers, and buyers and sellers near military bases are more willing to engage in the relatively burdensome process of financing a home purchase with a VA loan. This could be due to greater familiarity with the program or a desire to assist veterans and members of the military community.

We also found that in higher cost counties, utilization of the VA home loan program was lower than one would expect given the veteran population. This suggests that veterans may need greater assistance securing affordable housing in these areas, particularly in large coastal cities. More research is necessary to further explore the concentration in VA lending and the causal mechanisms for why proximity to military bases is so influential in loan choice.

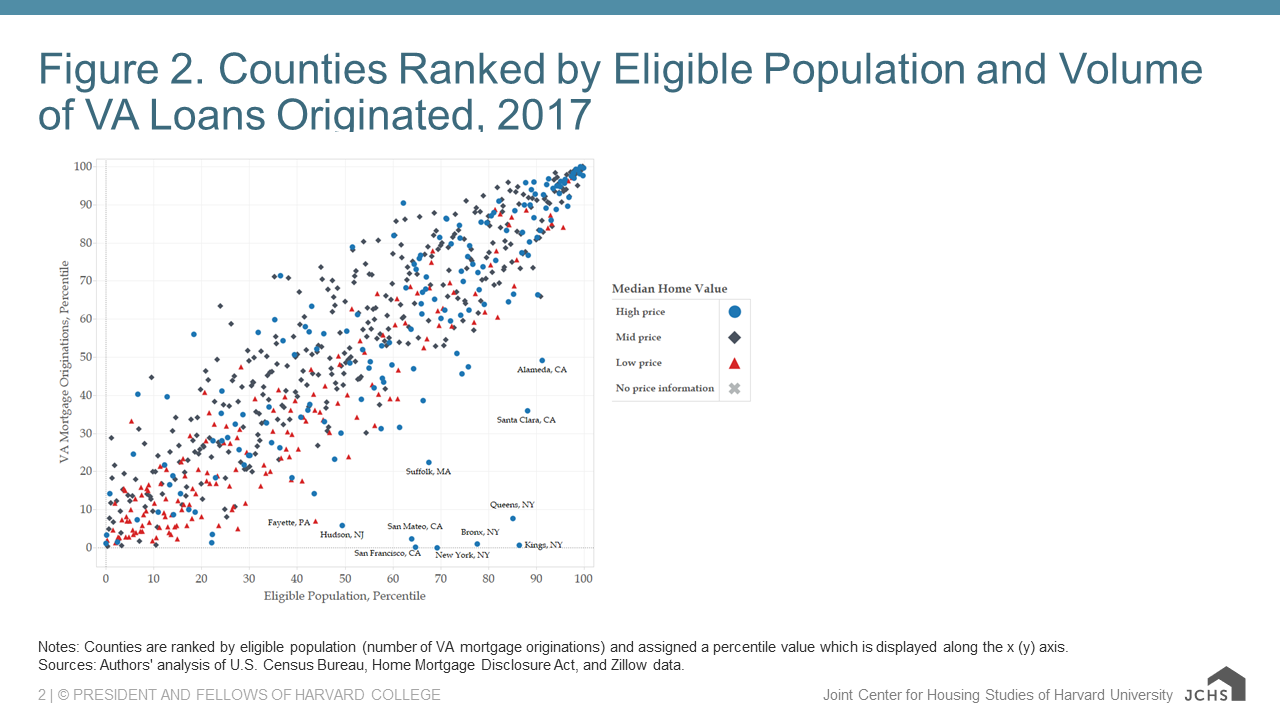

Figure 2: Counties Ranked by Eligible Population and Volume of VA Loans Originated, 2017

Sources: Authors’ analysis of U.S. Census Bureau, Home Mortgage Disclosure Act, and Zillow data.

Note: Counties are ranked by eligible population (number of VA mortgage originations) and assigned a percentile value which is displayed along the x (y) axis.

The views expressed here are those of the authors and not necessarily those of the Federal Reserve Bank of Philadelphia or the Federal Reserve System.