What Will Stop the Slide in Homeownership Rates? Keep Your Eye on Incomes.

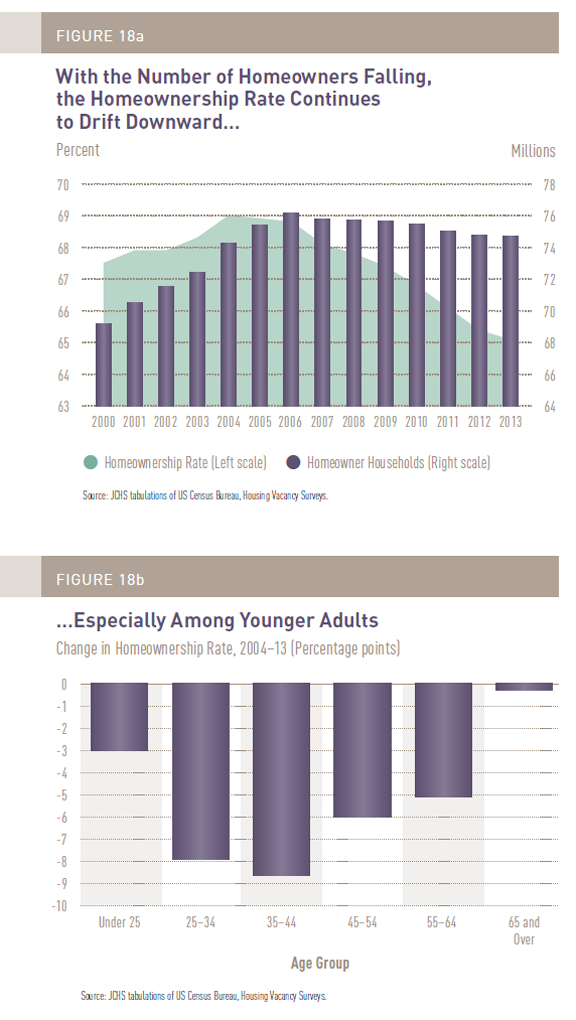

As highlighted in our new State of the Nation’s Housing report, the national homeownership rate declined for the 9th straight year in 2013 and now stands at its lowest point since 1995 (see Figures 18a and b, from our report, below). The falloff in homeownership has affected a broad range of demographic groups, but has been most severe among those in their late 20s through their early 40s, with their rates down at least 8 percentage points since 2004. In fact, while the overall homeownership rate is still slightly above the pre-boom rate of 64 percent, the share of households age 25-44 owning a home is at its lowest point since annual data became available in the early 1970s. Since these are prime ages for both first-time and trade up homebuyers, this substantial decline in owning has been an important reason for the continued weakness in the housing market.

Predicting when homeownership rates will stabilize—and possibly turn back up— must begin with an understanding of what’s been driving the downturn. There are many culprits. The dramatic fall in home values, which decimated housing wealth and forced millions into foreclosure, has made everyone far more aware of the financial risks associated with buying a home. Still, our analysis, and a variety of other surveys, indicate that the majority of young adults want to own a home someday. So changing preferences for owning would not seem to account for such a dramatic falloff in the homeownership rate over such a short period.

The incredible increase in the use of student loans is no doubt also a contributing factor. Between 2001 and 2010 the share of 25-34 year olds with student loans rose from 26 to 39 percent. And since 2010 the total amount of student debt outstanding has increased by about 40 percent. At the same time, however, the median amount owed among 25-34 year olds only rose from $10,000 to $15,000 between 2001 and 2010, which should not be a substantial deterrent to buying a home. Our analysis also found that the share of these young borrowers with high amounts of debt ($50,000 or more) rose from 5 to 16 percent, but this still a minority of all households in this age group. A recent Brookings Institution report came to a similar conclusion, finding that the median loan payment to income ratio has not exceeded historical levels. So while mounting student loan debt and increasing delinquency among these borrowers is not the main reason young Americans are deferring homeownership, it is certainly a factor.

Today’s far more restrictive mortgage underwriting standards are another limitation for those looking to buy a home. The decline in lending to borrowers with credit scores in the 600s has pushed up the average score for new borrowers well into the 700s. Since roughly half of all consumers have credit scores under 700, this is making it hard for many to qualify for mortgages. While there are some indications that lenders are starting to relax their standards, so far there hasn’t been much movement in the average score for borrowers.

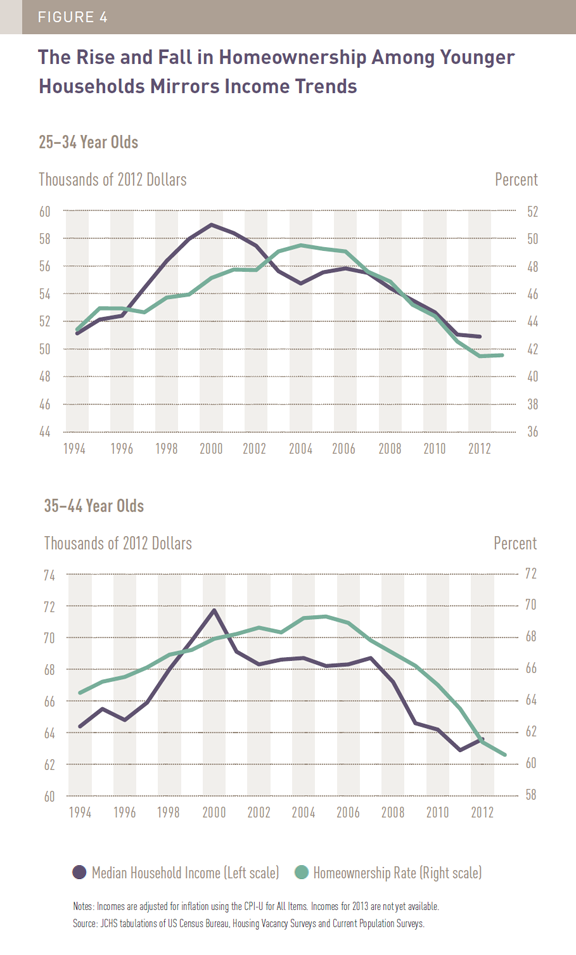

But at a fundamental level, it may not be necessary to look much further than trends in household incomes to explain the rise and fall in homeownership over the past two decades. Median household income for 25-34 year olds and 35-44 year olds grew sharply from 1994 through 2000, during a period when homeownership rates showed steady gains. Growth in homeownership then slowed as incomes softened during the mid-2000s (see Figure 4, from our State of the Nation’s Housing report, below).

While many blame lax underwriting for driving the homeownership rate boom, in fact much of the gains occurred during the 1990s when the economy was producing solid income growth. Since 2006, median household incomes have fallen substantially for those 25-44, with the homeownership rate declines mirroring these trends. In fact, just as the share of households 25-44 owning a home is as its lowest point since the early 1970s, the real median household income for this age group is at its lowest point since 1972. So, while young households are facing a number of headwinds to buying a home, until we see a resumption in income growth we are unlikely to see an upturn in homeownership rates.