The Negative (and Positive) Spillovers of Concentrated Foreclosure Activity in New York City

Foreclosures have negative effects not only for the people who lose their homes, but also for the neighborhoods where they lived.

In an article that recently appeared in Urban Affairs Review, Michael J. Lear, Elyzabeth Gaumer, and I conclude that, at least in New York City, neighborhood foreclosure activity during the peak of the Great Recession was associated with an individual property’s risk of foreclosure, but not in the way that most previous research has assumed. These findings suggest that financial institutions’ practices during the foreclosure process may have contributed to how quickly neighborhoods recovered from that crisis above and beyond the institutions’ roles in causing it. The research focused on two key phases in the foreclosure process, an early phase when a lender filed a foreclosure notice after a property owner missed some mortgage payments, and a later phase when properties were actually scheduled to be auctioned. (In New York, the latter process often occurs more than a year after the former one.)

Although New York City’s housing market fared better than many other markets during the recession, it was not immune to the problems associated with that downturn. Illustratively, in 2007 and 2008, there were nearly 14,000 foreclosure filings annually, double the number in 2004. In 2009, the number increased to over 20,000. The number of foreclosure auctions, however, was much smaller, ranging from 3,000 to 4,500 a year between 2007 and 2009.

This foreclosure activity was also highly concentrated. Between 2007 and 2009, over half of the city’s foreclosure filings occurred in just nine of the city’s 55 sub-borough areas (SBAs), all of them in Brooklyn or Queens. Moreover, over half of the city’s auctions took place in just six SBAs. Not all specific areas with the highest concentration of foreclosure auctions, however, were among the areas with the highest concentration of foreclosure filings. Rather, the share of foreclosure filings that result in scheduled foreclosure auction varied considerably across boroughs, from less than 10 percent being scheduled for auction in parts of Brooklyn to more than 40 percent in parts of Queens.

My coauthors and I hypothesized that the number of scheduled foreclosure auctions surrounding a property that had received a foreclosure filing is positively associated with the likelihood of that property itself reaching auction, net of other factors. Since foreclosure filings do not necessarily involved a transfer of ownership, however, we thought they might not have as strong an association as auctions may have.

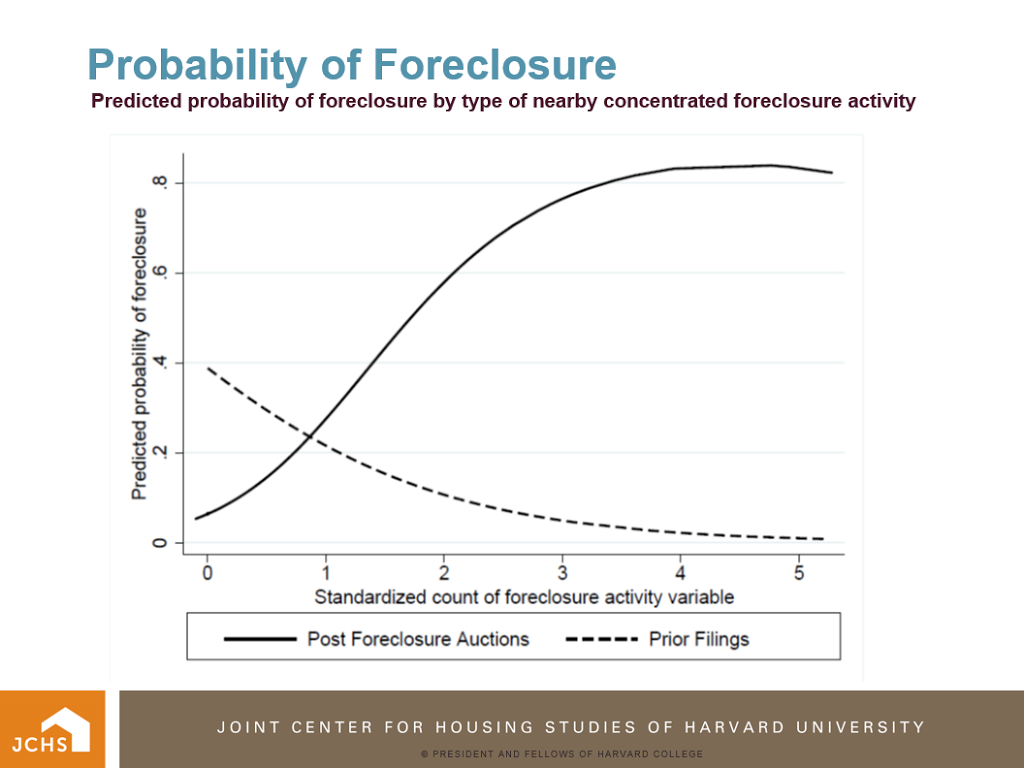

Drawing on data about individual property and neighborhood characteristics in addition to foreclosure activity, we found that levels of neighborhood foreclosure activity in both phases were, in fact, associated with an individual property’s outcome, but in different directions. Holding constant individual property and neighborhood characteristics, as the number of nearby properties with a foreclosure filing increases, the probability that an individual financially-distressed property will be scheduled for foreclosure auction decreases. This pattern is reversed for properties in the later phase of the foreclosure process. As the number of nearby properties scheduled for auction increases, the probability that an individual financially-distressed property will be scheduled for foreclosure auction also increases (See Figure).

These findings also suggest that at least in New York, banks and loan servicers may have delayed the processing of foreclosures in areas with larger numbers of properties with foreclosure filings. They may have done so because foreclosed properties may not sell as quickly or as profitably as in more desirable areas where there are fewer distressed properties and/or where foreclosed properties sell right away. Future research should examine these practices in more detail, not only in New York, but in other states as well and, in doing so, underscore the importance of financial institution practices not just in the lead up to the Great Recession, but throughout the recovery process as well.